Concept and types of regional taxes

The Tax Code authorizes regional legislative authorities to establish regional taxes, at the same time limiting their list in order to avoid overburdening taxpayers.

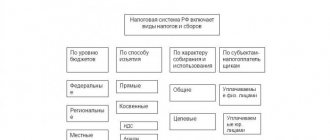

The taxation system of the Russian Federation is built in a certain way and consists of a number of levels:

- Federal;

- Regional;

- Local.

This level system made it possible to assign certain tax deductions to a specific budget (local, republican, federal).

Regional taxes are taxes, the establishment of which is provided for by the Tax Code of the Russian Federation and which are put into effect when one or another federal subject adopts the relevant law.

These taxes are subject to mandatory payment only on the territory of the relevant federal subjects.

The system of regional taxes includes taxes whose effect by tax legislation extends to the entire Russian territory, as well as those established by the laws of individual subjects of the federation. Payment of both is mandatory on the territory of these respective subjects by persons recognized by law as taxpayers.

The Federal Tax Code, Article 14, provides for only three taxes that subjects of the Russian Federation have the right to introduce on their territory. Regional taxes include:

- on property collected from organizations;

- for gambling business;

- transport.

The concept of local taxes and fees

Local authorities are also given limited powers by domestic legislation to establish local taxes and fees in the territory under their control.

The granting of such powers is due to the inability to fully ensure the interests of the basic municipal districts at the expense of the republican and regional budgets, which is why local taxation and the formation of the local budget are designed to ensure the local interests of the population and the territorial unit as a whole and to promote its development.

Local taxes and fees are mandatory payments that are established by the local authorities of the basic administrative-territorial unit within the limits of the rights and powers granted to such authorities by federal tax legislation and the Tax Code of the Russian Federation.

Like federal and regional, local taxes and fees are included in the taxation system of the Russian Federation.

The nature of such taxes and fees does not differ from other obligatory payments payable to the budgets of higher levels; they have a pronounced fiscal nature and are designed to provide financial expenses for the municipal budget.

Composition of regional taxes

As noted above, regional taxes include:

- taxes that apply to the entire territory of the Russian Federation in accordance with federal laws on taxes and fees, as well as the Tax Code of the Russian Federation;

- taxes established by the legislative bodies of independent constituent entities of the Russian Federation, which are valid only on the territory of the corresponding constituent entity.

Until the modern Russian Tax Code was put into effect, the domestic tax system was characterized by the division of regional taxes into:

- mandatory;

- optional.

The essence of such a division was the possibility of limited application in regions (regions) of taxes separately established on the territory of the country. Local government authorities were empowered to impose taxes of regional significance in those quantities that they considered necessary independently without any restrictions. Some subjects of the federation, due to the exercise of such powers by the authorities, were overloaded with taxation to the maximum.

The current Tax Code of the Russian Federation was intended to limit the tax burden and bring the taxation system throughout the country into a single state. It was he who established an exhaustive (closed) list of regional taxes that have the right to be introduced in individual regions by local laws, thereby reducing the unaffordable tax burden on taxpayers.

From now on, it is prohibited to establish additional regional taxes that are not included in the Tax Code of the Russian Federation, which has a beneficial effect primarily for business entities - legal entities.

Features of local taxes and fees

Despite the similarity of local taxes and fees with the general characteristics of the entire Russian tax system, local taxes and fees have their own distinctive features:

- funds received by the relevant local budget are subject to spending exclusively on the needs of the municipality itself;

- local withholding taxes are accumulated in the local budget; higher budgets at the regional or federation level are distributed in certain proportions between all three levels, including the local one.

- the decision to introduce and collect appropriate fees lies solely with local authorities;

- control over the use of local budget funds is also carried out locally by self-government bodies.

- a wide range of powers for the legal regulation of local taxation, which includes the ability to reduce tax rates and establish benefits and privileges for certain categories of tax payers.

Elements of regional taxes

Regional taxes are recognized as a set of taxes established throughout the territory of the Russian Federation by its laws and the Tax Code in particular, as well as on the scale of a single region, but taking into account the provisions of the current federal tax legislation.

Both levels of taxes include separate, narrower classifications; in particular, for regional taxes, the classification is represented by a list of taxes that can be established within a subject by its bodies:

- property tax;

- gambling tax;

- transport tax.

An analysis of existing regional taxes shows that for the most part, the taxpayers are legal entities - organizations engaged in economic activities, and in rare cases individuals.

Characteristics of regional taxes

The characteristics of regional taxes depend on a particular tax introduced in the region. In general, each of the types allowed for introduction within the region is characterized by the following:

1. For the property tax of a legal entity, it occupies the most significant layer in the regional taxation system. On average, regional budget revenue is generated by paying this tax by 6% or more.

Taxpayers are legal entities on whose balance sheets there is property that, according to tax legislation, is regarded as an object of taxation.

The objects in this case are movable and immovable property for domestic legal entities, which, according to accounting, are accounted for as fixed assets of the organization.

For foreign legal entities engaged in economic activities in Russia through representative offices, the object is recognized as movable and immovable property, which is also fixed assets according to financial statements, as well as property received under a concession agreement.

If a foreign enterprise does not carry out its activities through representative offices in the Russian Federation, then the object is real estate in Russia, which is the property of this organization, as well as property received under a concession agreement.

2. For the tax on gambling business, taxpayers are legal entities or individual entrepreneurs whose business activities are related to generating income in the field of gambling business by charging fees for gambling, betting, etc.

The objects of taxation are tables, machines recognized as gaming, as well as betting or bookmaker's office cash desks.

Each unit of the specified object must first be registered with the territorial tax service.

In this case, the registration period is 2 or more days before the day of installation (opening of an office or betting shop) for each individual unit.

To register, the taxpayer must submit an application, after which a certificate of the appropriate uniform form is issued.

3. Transport tax is regional, with characteristic features.

Thus, the object of taxation:

- motor vehicles;

- motorcycles;

- scooters and others, including watercraft and aircraft that have been registered on the territory of the Russian Federation in the manner prescribed by its legislation.

Taxpayers are individuals in whose name the specified objects are registered. This category of regional taxes contains a fairly large list of persons who are granted benefits for paying this tax.

Transactions not recognized as objects of taxation

Existing tax authorities establish certain types and a list of transactions that, for one reason or another, cannot be recognized as a full-fledged object of taxation . This concept means that these transactions and the fact of their direct implementation cannot entail the obligation to pay tax payments, as well as other established fees, for example, VAT .

Transactions not recognized as subject to taxation include the following types :

- operations for the transfer of certain objects of socio-cultural or housing and communal services into the ownership of state bodies or local governments free of charge. At the same time, the concept of objects of social, cultural and housing and communal purposes may include: residential buildings, recreational facilities, kindergartens, as well as electrical substations, water intake structures, gas buildings and complexes, and other types of similar buildings;

- transfer of property to state or municipal enterprises in the manner of privatization buyout;

- performance of certain works, or provision of prescribed services by state and municipal bodies, in the exercise of their exclusive powers, in a certain field of activity. An important point is the fact that the responsibilities for performing the above actions should be assigned to state or municipal bodies by the legislation of the Russian Federation, or the laws of the constituent entities of the country, as well as by order of local government bodies;

- transfer of certain goods, provision of services, or performance of work to state authorities or local government on a free basis. In addition, these types of goods or services can be transferred to the ownership of municipal institutions, as well as unitary enterprises;

- operations for the transfer of land plots, or for replenishing the endowment capital of a non-profit institution free of charge;

- other types of transactions, the terms and conditions of which will not allow them to be recognized as an object of taxation , including payment of VAT .

Functions of regional taxes

Regional taxes are funds paid by legal entities to the regional budget, which allows the subsequent subject of the federation, represented by its governing body, to use these deductions to perform a number of functions:

- accumulation and use of funds received by the regional budget to achieve regional goals;

- the exercise by regional authorities of their representative and administrative powers;

- self-sufficiency in the implementation of programs of social significance developed and operating within the territory of the region (region);

- development of the region's infrastructure;

- maintaining the environment and natural resources, since they are the natural basis for the existence, development and prosperity of the region.

- stimulating business activity, carrying out structural reforms that will make the region (region) more attractive in terms of investment, which will subsequently have a positive impact on the future well-being of the regional budgetary and tax sphere.

The importance of regional taxes

The importance of regional taxes in the budgets of the constituent entities of the Russian Federation is colossal. This is because modern realities entrust them with the function of a lever regulating the uninterrupted formation and replenishment of the regional budget.

The main role of regional taxes is that they are designed to materially provide and nourish the regions. These material resources are subject to redistribution and direction for the benefit and development of the region, solving primary problems and implementing socially significant programs that are not financed from the federal budget or are financed in a significantly smaller amount than necessary.

The regional government, thanks to such taxes, as well as benefits and sanctions that complement the taxation system within the region, has an impact on legal entities and their economic behavior, thereby maximally leveling the conditions for all participants in social reproduction.

The procedure for establishing regional taxes

The introduction of regional taxes and their termination in the territories of federal subjects is carried out on the basis of the provisions of the Tax Code of the Russian Federation and the territorial laws of the subjects of the Russian Federation governing taxation issues.

Legislative bodies of state power of a federal subject, when establishing taxes for their region (region), are guided by federal tax norms concentrated in the Tax Code of the Russian Federation. They also define:

- tax rates;

- payment procedure;

- payment terms.

The remaining elements of taxation, as well as the range of taxpayers, are provided for by the Tax Code of the Russian Federation itself.

The regional legislative power, specified by the laws, taking into account the provisions of the Tax Code of the Russian Federation, can additionally provide for tax breaks (benefits) for certain categories of taxpayers, as well as the procedure and grounds for their application.

Principles of local taxes and fees

Local taxes and fees exist and operate according to the general principles of the entire tax system of the country. These include the following principles:

1. The principle of justice. When introducing a particular tax, the existence of an objective opportunity for the target group of taxpayers to pay the tax (fee) must be taken into account;

2. The principle of universality and equality of taxation. The obligation to make payments to the budget, if there are legal grounds, lies with an indefinite circle of persons who are equal in their rights and responsibilities. It is not permissible to unjustifiably exempt some payers from paying a tax (fee) and simultaneously collect it from others under the same conditions.

3. The principle of economic feasibility. The establishment of taxes cannot be spontaneous and arbitrary, but must be justified from an economic point of view. Their introduction should not infringe on the rights and freedoms of citizens provided for by the Constitution of the Russian Federation.

4. The principle of unity of the economic space of the Russian Federation. Taxes (fees) that in any way encroach on the integrity of the country’s economic space are unacceptable. Mandatory payments to the budget cannot directly or indirectly affect the freedom of movement within the country, both goods (works, services) and financial resources. Any obstacle to legally permitted business activities by introducing mandatory payments is prohibited.

5. The principle of compliance with the procedure for establishing a tax (fee). Taxes (fees) that are not provided for in the Tax Code of the Russian Federation or are introduced in violation of the procedure are not subject to payment.

6. Certainty of tax liability. By regulation, when the obligation to pay to the budget is introduced, all elements of taxation must be fixed. The wording of tax legal norms must be clear so that the taxpayer clearly knows for what, how much, and when the corresponding tax is required to be paid to the budget.

7. Presumption of interpretation of tax doubts in favor of the taxpayer. If there are vague formulations and doubts about tax rules, their interpretation is carried out in favor of the taxpayer.