general characteristics

The key grouping of tax obligations implies the division of all budget payments into two large groups: direct and indirect taxes, a list of which is given below. Let's understand the key concepts.

Thus, direct liabilities should include all payments that are levied directly from the taxpayer’s property assets or from the income he receives. In other words, the taxpayer independently calculates and pays tranches to the budget. Moreover, transfers are made at the expense of the property owner’s own funds or income. Examples of such non-commercial organizations can be: personal income tax, non-commercial tax liability, obligations for property, transport, land plots and other assets.

Indirect taxes include a liability that is not calculated directly against the tax base, but is included in the cost of goods, work, or services sold or purchased. In simple words, the seller, when determining the final selling price of the goods, lays down a certain tax liability tariff. Consequently, indirect taxes are levied on the buyer when making payments for the purchased goods. It is the buyer who pays the additional tariff included in the price. After which this tariff, paid by the buyer, is transferred by the seller of goods to the budget.

In other words, the key difference is the nature of the withdrawal. That is, direct fees are applied specifically to the property or income-generating assets of the taxpayer. And indirect ones are calculated as a certain allowance. In most cases, the premium is set on the cost of the assets or services being sold. However, fixed payments can also be classified as CN, which are determined regardless of the tax base.

Direct taxes: types and features

Direct taxes include fees that the state levies on the income of citizens (salaries, profits, interest) or their property (land, real estate, vehicles). This proposed type of fee is paid by the citizen independently to the state treasury.

The system of direct taxes of the Russian Federation includes the following types:

from legal entities:

- at a profit;

- on property;

- to the ground;

- for business (for example, in the field of slot machines);

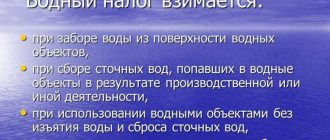

- to water sources;

- for mining.

from individuals:

- income;

- property;

- from property;

- transport;

- on property received by a citizen by inheritance or gift.

The amount of direct taxes is completely determined by the level and size of a citizen’s income. For example, as wages increase, the amount of contributions increases.

The main objects of taxation when calculating this type of fee are:

- total or taxable income;

- total or taxable value.

What is indirect tax: definition

In fact, an indirect tax is an additional tariff that the seller included in the cost of the goods or services sold. However, the buyer has to pay this extra charge. The seller is just an intermediary who sets the markup and pays it to the budget upon completion of settlements.

We can also say that indirect taxes include consumption obligations. That is, such payments to the budget are made from objects purchased for one’s own needs, that is, for consumption needs. Such obligations are also called consumption charges.

Now let's determine which tax is indirect?

Indirect taxes on business and individuals from the state's point of view

Compared to direct taxes, collecting indirect taxes seems to be a simpler task for the state. In this case, the main taxpayer is business, and the tax base is sales revenue or added value, i.e. indicators that are easy to monitor during an audit.

An enterprise may not make a profit for some time or may not own (rent) real estate, but added value is almost always generated if at least some activity is carried out. Individuals may not be payers of personal income tax (for example, pensioners), but in any case they indirectly pay indirect taxes included in the price of purchased goods.

Therefore, we can say that, unlike direct taxes, indirect taxes are obligatory for payment by all economic entities on the territory of the state.

In addition, because These taxes are paid on turnover, then in the presence of inflation, the amount of tax payments “automatically” increases in proportion to the rise in prices.

Therefore, in countries with a relatively high level of inflation and difficulties in tax administration (which includes Russia), the ratio of direct and indirect taxes, as a rule, shifts in favor of the latter.

Types of indirect taxes

According to the current fiscal legislation, officials have determined which taxes are indirect. Thus, Chapters 21 and 22 of the Tax Code of the Russian Federation establish key rules for the application of VAT and excise taxes. It is these payments that are considered indirect taxes that must be paid to the budget.

Please note that all non-residents are credited to the federal budget. That is, tax rates and procedures are established by the Government of the Russian Federation.

In addition to VAT and excise taxes, other tax payments are paid to the state: customs duties and indirect business taxes. Let's look at the features of each BUT in more detail.

Table of direct and indirect taxes

All types of taxes can be summarized in a table:

| Type of tax | Tax name | Budgets | ||

| federal | regional | local | ||

| Direct taxes | For individuals | |||

| Personal income tax | v | |||

| Property tax | v | |||

| Transport tax | v | |||

| Land tax | v | |||

| Water tax | v | |||

| For legal entities | ||||

| Income tax | v | |||

| Personal income tax from employees | v | |||

| Property tax | v | |||

| Transport tax | v | |||

| Land tax | v | |||

| MET | v | |||

| Gambling tax | v | |||

| Water tax | v | |||

| Trade fee | v | |||

| Indirect taxes | VAT | v | ||

| Excise tax | v | |||

VAT

The most common tax obligation, which is established for almost all types of goods, works or services sold in the territory of our strata. VAT is also used when determining the cost of goods when imported into Russia from other countries.

The VAT rate has three key values: 0% - preferential, 10% - for a certain type of product, 20% - applies to all other goods.

As we noted above, obligations are paid by buyers of goods, works, and services sold. However, this BUT has a mandatory condition - the presence of an intermediary between the buyer and the state budget. The seller acts as this intermediary.

What taxes are indirect?

Surely, you have heard terms such as direct and indirect taxation from eminent economists and financiers.

What taxes are classified as indirect and why they are called that - we will look into this. How is indirect tax collected?

A tax of this type is established in the form of a surcharge on the price of products or on the tariff for services and work, in contrast to a direct tax levied directly on the taxpayer’s income. The business owner sells his products, adding a premium to the price by the amount of the fee, and then transfers it to the budget. In essence, the payer of such a tax is the consumer who buys a product or orders a service, and the enterprise or entrepreneur acts as its collector.

According to leading experts, indirect taxes suppress citizens' desire for self-government, since they are collected hidden. Whereas a direct tax is clearly visible to anyone whose income is calculated, so it stimulates a more active civic position in society.

Types of indirect taxes

Official economics distinguishes three types of indirect taxes: excise taxes, customs duties and various fiscal monopolies.

Excise taxes are set as a percentage of the selling price of most highly profitable goods. By the way, according to this classification, excise taxes also include VAT.

Customs duties are paid at border crossings in the process of exporting or importing goods. Separate duty rates are established for different groups of goods.

Fiscal monopolies are payments to the government for its services. For example, a license fee or state registration fee.

Russian indirect taxes

In the Russian Federation, indirect taxation is actively used by the state to replenish the country's budget.

VAT is charged anywhere and everywhere: at every stage of production and circulation of goods. It represents a percentage markup on value added. The taxpayer pays to the budget the difference between the VAT received from the buyer when paying for his products or work and the VAT paid to suppliers and contractors for goods, materials and services. And, despite the fact that this is also essentially an excise tax, we usually consider it separately.

Excise taxes in our country represent a high percentage markup on the price or a certain amount established per unit of measurement of a certain group of goods. In Russia, these are alcohol, tobacco products, alcohol-containing products, jewelry, cars and gasoline.

Customs duties (export and import) are a separate type of indirect taxes. They are paid by the taxpayer engaged in foreign economic activity.

State duties and fees are collected from the taxpayer when he carries out actions that require special state registration. Fees when registering an entrepreneur or enterprise, when making changes to the Unified State Register of Legal Entities, fees when obtaining a license to carry out a specific type of activity, etc. The manufacturer must include all these costs in the cost of its products.

Insurance premiums of individual entrepreneurs, by the way, are also an example of indirect taxation, since their total accrued and paid amount is allowed to be attributed to production costs. Under normal market relations, contributions are also included in the sales price of products or services and, in fact, a specific consumer becomes their payer.

The lion's share of all budget tax revenues of the country comes from indirect taxes. Whether this is good or bad is for eminent economists and financiers to decide, but it turns out that the bulk of all taxes in the country are paid by the end consumer.

Excise tax

An obligation that applies only to certain types of goods and manufactured products. For example, excise taxes are included in the price:

- gasoline;

- ethyl alcohol;

- cigarettes;

- alcohol;

- passenger cars;

- alcohol-containing products;

- diesel fuel.

There is no single rate for excise taxes, since the value is set on an individual basis. That is, separately for each group of excisable products. Moreover, the values are approved for the calendar year and for the next 2 years.

Types of bets

Duty rates are expressed in monetary terms, either in domestic or foreign currencies. They are established in some relation to the customs price of goods transported across the border of the Russian Federation. When determining them, the provisions of the Federal Law “On Customs Tariffs” are taken into account. Tariffs are the same for all entrepreneurs, and therefore do not change under the influence of various factors, unless otherwise provided by law.

Attention! The Federal Assembly of the Russian Federation is engaged in setting maximum rates of import duties, for which trade and political relations with different countries are taken into account.

Customs duties

Payments paid by companies and individual entrepreneurs importing goods into the territory of the Russian Federation. Indirect taxes are not characterized by a fixed tariff rate. The volume of payments for customs duties is determined exclusively from the current terms of agreements concluded between the Russian Federation and importing countries.

Calculations are made on the basis of declarations filled out by importers. Let us remind you that when importing products into our country, you must submit a declaration in the prescribed form no later than 15 days from the date of import.

Special types

There are several other rates that are charged by customs officers of countries that are members of the Customs Union.

Table 1. Classification.

| Type of bet | Peculiarities |

| Special | Designed to protect the country's domestic market from excessive amounts of imported goods. Therefore, a higher rate applies to certain groups. |

| Anti-dumping | It is used to bring the prices of imported goods to the level available in the country. But it is effective if its use does not cause any harm to domestic producers. |

| Compensatory | This duty is added to regular fees, which reduces the competitiveness of goods imported from other countries. Therefore, buyers prefer to purchase products created by domestic companies at reduced prices. |

| Seasonal | They are introduced for a maximum of 6 months and are also intended to regulate exported goods. An exact list of the goods themselves, as well as information about the applicable seasonal rate and duty payment rules, are approved by the Russian Government. They are usually used instead of ETT rates. |

Attention! Art. 79 of the Customs Code of the Customs Union contains information that customs duties help reduce the harm caused to the country’s domestic economy by imports.

Watch the video for everything on the topic:

The above duties are not a customs payment, therefore they are established only on the basis of a decision made by the EEC Board. If businessmen refuse to pay these duties, they are subject to administrative liability. But in practice, there are situations when companies win court proceedings because they have proven that there are no grounds for using anti-dumping measures.

State fees

This type of fees can also be classified as indirect payments to the budget. Why? A state fee is charged for a specific legal service provided by a government agency. The payment is optional, meaning it is paid only when the taxpayer needs to complete a specific legal action. This means that state duty cannot be attributed to direct budget tranches.

Also, the size of the state duty has fixed values, which are established regardless of the property and material characteristics of the economic entity.

VAT in the Russian Federation

Value added tax is paid unless legislation exempts a Russian business entity from paying it. An example would be UTII or simplified tax system.

VAT is calculated as a percentage of the price of a product or service. There are several rates in the Russian Federation: 18%, 10% and zero.

A rate of 10% is established in relation to the following services and goods:

- Food products

- Medical purpose

- Air transport services

- Children's products

- Periodicals

- Purchasing breeding stock