What is property tax

Property taxes are paid by taxpayers on taxable objects that they own. These fully include the property tax of individual entrepreneurs.

Property subject to taxation

Every entrepreneur is a payer of personal property tax if he has machines, buildings, equipment and other objects subject to it. The list of objects subject to this tax also includes:

- Residential buildings, including dachas and garden houses;

- Apartments and rooms;

- Garages;

- Unfinished construction projects;

- Other non-residential buildings and premises.

Important! According to Article 401 of the Tax Code of the country, and in particular its paragraphs 1 and 2, property included in the common common property in apartment buildings is not subject to tax.

This includes staircases, basements, and so on.

Objects of taxation and rates

When calculating property taxes, the cadastral value is used. The property of the entrepreneur is considered as an object:

- Housing: house, apartment, room.

- Unfinished construction.

- Garage buildings.

- Any other objects for which ownership is registered.

New legislation regulating the procedure for paying property tax for individual entrepreneurs in 2020 establishes that the cadastral value of the property is used to calculate the amount of the fee. Before the adoption of the relevant articles of the Tax Code, the property had an inventory valuation that was much lower. Accordingly, the property tax for individual entrepreneurs in 2020 was significantly increased than, for example, in 2014–2015.

The rate can be changed up or down, but does not exceed 2% of the calculated base. The annual amount of property tax is paid by October 1.

Should the individual entrepreneur pay it?

The procedure for taxing the property of individuals is regulated by the Tax Code, which is considered federal law, with all adopted amendments and recent additions. This issue is addressed in Chapter 32 of this document “Property Tax for Individuals”. Sole proprietorships fall into this category.

How to calculate income over 300,000 individual entrepreneurs on UTII and simplified tax system - what tax is paid

Picture 2 Work to increase business profitability

An entrepreneur pays property tax if the following conditions are met:

- He is the owner of the property.

- The property is located on Russian territory.

If the property is rented, that is, it is not documented to be the property of the entrepreneur, then tax should not be charged on it.

Note! When real estate owned by an entrepreneur is located in another state, it is not subject to property tax in Russia.

At the same time, the amount of individual entrepreneur tax on real estate depends on the choice of taxation regime. He can be:

- General.

- Special.

The following features of its payment are highlighted:

- An individual enterprise operating under the UTII system, having a patent or being simplified, pay tax on real estate based on their cadastral value, provided that a special law has been adopted in the region.

- When working under the Unified Agricultural Tax, there is no need to accrue and pay this tax.

Payment of tax not according to the cadastral list

If the property is not included in the regional cadastral list, and the individual entrepreneur uses a special tax regime, you do not need to pay anything . Users of the general taxation system are required to pay contributions even in respect of property not included in the cadastral list.

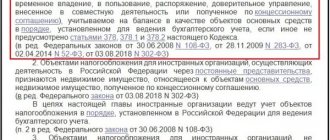

This very list of real estate is specified in paragraph 1 of Art. 378.2 Tax Code of the Russian Federation. All property in this list is approved as of January 1 of the current Tax period.

The procedure for paying property tax included in the cadastral list and not included there is no difference . In addition, the law of the region may provide for a separate opportunity to obtain an individual entrepreneur’s property tax benefit in the form of an exemption from its payment.

This is possible if the area of the administrative, business or shopping centers is less than that established by law or its cadastral value does not exceed the minimum established by the legal act.

You can also find out whether real estate is classified as cadastral or not by making a request to the tax authorities . To do this, you can request from Rosreestr an extract from the cadastre for the estimated value of the property. The owner has the right to seek exclusion of property from the cadastre list through the court.

When 30% of the total area of the entire building is used for office space, it is considered to be an administrative and business center, which, in turn, belongs to the cadastral list of objects.

All this must be taken into account before paying taxes, as well as the fact that the tax office commits quite a lot of violations in this regard. If necessary, you need to defend your rights through the court and legally receive a tax benefit.

Most individual entrepreneurs use special taxation systems that provide tax benefits in the form of exemption from paying individual contributions to the budget.

Individual entrepreneurs in all taxation systems, except the general one, do not have to pay property tax on all real estate, except for that which is included in the officially approved list of property by cadastral value.

Payment rates

Payment deadline for the simplified tax system for individual entrepreneurs - when to submit a declaration

According to the law, the rate of property tax is determined by municipal authorities. But at the same time its value should not be higher than 2%. The calculation is carried out by the executive bodies of the federal tax service in the given area. The results of this accrual are sent to each individual entrepreneur in the form of a notification once a year. Payment is made for the previous reporting year. The deadline is the same for all individual taxpayers. The deadline is early December next year.

Payment of property taxes

3-NDFL for individual entrepreneurs - what is it, sample form and when to submit

When purchasing real estate, an individual entrepreneur, unlike ordinary enterprises, registers it as the property of an individual. In the course of his activities, such a citizen is responsible for his actions with his own property. Even if a citizen decides to close an individual entrepreneur, it will not cease to remain in his possession. In case of death, all property is inherited.

Permanent accounting

When registering his rights to acquired property, the head of the individual entrepreneur acts as an ordinary citizen. Therefore, his rights can only be challenged through an arbitration court.

In their work, individual entrepreneurs most often use the simplified tax system; it allows them to simplify accounting. But when purchasing expensive real estate, the simplified procedure does not allow you to receive benefits such as a property deduction for individual entrepreneurs. To do this you will have to pay personal income tax.

The peculiarity of the simplified taxation system is that the tax is calculated based on income from the sale of all types of goods and services. When determining the base for calculating the tax, the taxpayer can receive a property tax deduction from the sale of housing, houses, including in garden partnerships, and land plots that have been in his ownership for no more than three years at the time of payment, but not exceeding one million rubles.

This also applies to other real estate objects owned by an entrepreneur for less than three years in an amount of no more than 250 thousand rubles.*

When talking about whether an individual entrepreneur can receive a property deduction when buying an apartment, you need to focus on these circumstances.

Important! If the premises are used for commercial activities, there is no tax deduction when selling it.

Submitting an application to use a property

If property tax is paid, then individual entrepreneurs using the simplified tax system in 2020 have the opportunity to use preferential conditions, as contained in the Tax Code of the Russian Federation - Article 407. The following

are exempt from the obligation to pay property tax:

- Minor children who are orphans and left without parental care.

- Large families recognized at the legislative level.

- Persons who have dependent disabled children, except those who are fully supported by the state.

If an entrepreneur has the right to use benefits, then he must write a free-form application, attach documents confirming this and personally take all this to the tax inspector.

To use benefits, a package of documents must be provided to the Federal Tax Service, which serves as confirmation.

Based on the Federal Law, individual entrepreneurs who have just completed the registration process and started working have the right to take advantage of a zero tax rate for up to two tax periods. These “vacations” exempt the business owner from certain mandatory deductions. The zero rate includes income and property tax and VAT. The entrepreneur must pay everything else.

It is worth considering that such benefits are not provided for everyone; to receive them you must meet certain criteria:

- IP registered for the first time. Only beginners can use tax “vacations” in their work. It is prohibited to liquidate an old business, open a new one and then claim preferential conditions.

- For the taxation system, a patent or simplified tax system is used. Other systems are not included in this case.

- A business must be opened in one of three areas: production, scientific, social.

Benefits are not used equally throughout Russia. You can only count on receiving them when they are accepted by local authorities at the regional level.

We recommend you study! Follow the link:

Property tax for individual entrepreneurs in 2019

Do I need to pay tax when buying an apartment?

When purchasing housing, not all entrepreneurs can receive a tax deduction. To do this, the following conditions must be met:

- Have confirmed income on which personal income tax is paid at the rate of 13%.

- A declaration in form 3-NDFL must be submitted and submitted to the tax office no later than April 30 after the reporting year. It reflects the amount of deduction that the entrepreneur claims.

- In some cases, a certificate of form 2-NDFL is additionally submitted.

- A package of documents confirming the rights of the owner.

- Confirmation of registration of the apartment as the property of the entrepreneur himself or his family members.

Note! Now the maximum amount of tax deduction when buying an apartment is 260 thousand rubles* and you can get it once in your life.

What types of real estate are eligible for tax deduction?

Private entrepreneurs, like other citizens, can receive a tax deduction for the following types of expenses:

- Standard. They are available to needy citizens upon application or submission of a declaration.

- Social. Given for education or medical services. Sometimes this is compensation for insurance and pension payments.

- Investment. In the form of a financial payment to the account upon the sale of securities that were owned by the individual entrepreneur for more than three years. In this case, there are restrictions on the amount.

- Professional. Related to the receipt of income of an entrepreneur or individual in the amount of documented expenses.

- If it is impossible to confirm expenses, you can exercise your right to a deduction in the amount of 20% of the total amount of income from business activities. This can only be done by persons officially registered as individual entrepreneurs.

- Property. They can be obtained by selling real estate, land and other property.

Individuals can use a professional deduction if the property compensation amount is less and it is possible to confirm expenses.

Tax office: paperwork

Difficulties with processing tax deductions may arise in the following situations: In the absence of documents confirming expenses; Payment made by another person. Using the services of organizations that do not have a license.

In these cases, the possibility of obtaining deductions is minimal.

Property tax for individual entrepreneurs on the simplified tax system

Individual entrepreneurs may not pay property tax for individual entrepreneurs using the simplified tax system. However, this only applies to properties that are used in commercial activities and are included in the list of special objects. That is, using the simplified system, an entrepreneur must pay tax on the following property:

- not used in direct activities;

- involved in the production process, but is paid according to the cadastral valuation.

Note! The problem may arise when it is impossible to separate property into: personal and work.

For example, the office may be located in the apartment of an entrepreneur, and his car is used both for the needs of the owner and for transporting goods. The tax authority does not take this into account. The calculation is carried out according to the available information.

Benefits for property owners

Benefits for individuals have been approved at the legislative level. The categories of persons in respect of whom there is an exemption from paying tax are presented in Art. 407 Tax Code of the Russian Federation. The benefits for individuals apply to individual entrepreneurs who own property.

If the property is involved in the entrepreneurial activities of an individual entrepreneur, the exemption does not apply.

Subjects of the Federation are given the right to determine real estate in respect of which tax relief is used. Regions independently select the objects that are granted exemption. In a predominant number of cases, the property relates to objects of social significance (operating, for example, to provide medical services), administrative buildings of production and other similar types.