Application for Unified Agricultural Tax when creating a peasant farm

In order to tax peasant farms under the Unified Agricultural Tax, it is necessary to switch to this special regime.

To switch to the Unified Agricultural Tax, you need to submit a corresponding notification to the tax office no later than December 31 of the year preceding the calendar year from which this special regime will be applied (clause 1 of Article 346.3 of the Tax Code of the Russian Federation). Notification form No. 26.1-1 was approved by Order of the Federal Tax Service dated January 28, 2013 No. ММВ-7-3/ [email protected]

In this case, you need to take into account the general rule: if the deadline for submitting a notice falls on a weekend or a non-working holiday, it will be possible to submit a notice on the first working day following such a day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation). So, for example, to switch to the Unified Agricultural Tax from 01/01/2019, a notification can be submitted until 01/09/2019 inclusive.

A newly created peasant farm for the application of the Unified Agricultural Tax can submit a notification of transition to a special regime no later than 30 calendar days from the date of registration as an organization or individual entrepreneur. In this case, the unified agricultural tax is applied from the date of registration of the organization or individual entrepreneur (clause 2 of article 346.3 of the Tax Code of the Russian Federation).

Taxation of heads of peasant farms under the general regime. I can’t figure out whether it is necessary to pay personal income tax on income if the head produces agricultural products, the share of which exceeds 70%{q} What confuses me is that agricultural producing organizations pay income tax at a rate of 0%, and the head must pay 13% .

In accordance with paragraph 1 of Article 1 of the Federal Law of June 11, 2003 N 74-FZ “On Peasant (Farm) Economy” (hereinafter referred to as the Law on Farming), a peasant (farm) enterprise is an association of citizens related by kinship and (or) property who have property in common ownership and jointly carry out production and other economic activities (production, processing, storage, transportation and sale of agricultural products), based on their personal participation.

Clause 2 of Art. 1 of the Law on Farming establishes that a farm can be created by one citizen. In accordance with paragraph 2 of Art. 23 of the Civil Code of the Russian Federation, the head of a peasant (farm) enterprise operating without forming a legal entity is recognized as an entrepreneur from the moment of state registration of the peasant (farm) enterprise (hereinafter - peasant farm).

According to Article 15 of Federal Law N 74-FZ, each member of a peasant farm has the right to a portion of the income received from the activities of the farm in cash and (or) in kind, fruits, products (personal income of each member of the farm). The amount and form of payment of personal income to each member of the farm are determined by agreement between the members of the farm.

In accordance with paragraphs. 14th century 217 of the Tax Code of the Russian Federation, the income of members of a peasant (farm) enterprise, received in this enterprise from the production and sale of agricultural products, as well as from the production of agricultural products, their processing and sale, is not subject to taxation - for a period of five years, counting from the year of registration of the specified enterprise.

After five years after registration of a peasant (farm) enterprise, taxation of the income of members of the enterprise must be carried out in the generally established manner, and taxation of the income of the head of the enterprise - in the manner established by Chapter. 23 of the Tax Code of the Russian Federation for individual entrepreneurs.

Income received from business activities is indicated on sheet B of the Personal Income Tax Declaration. This sheet is filled out by individual entrepreneurs, including those who are the heads of peasant (farm) farms.

https://www.youtube.com/watch{q}v=subscribe_widget

In paragraph 4 “For the head of a peasant (farm) enterprise” of Sheet B it is indicated: in subparagraph 4.1 - the year of registration of the peasant (farm) enterprise (150); in subparagraph 4.2 - the amount of income not subject to taxation in accordance with paragraph 14 of Article 217 of the Code ( 160)

Recalculation of taxes upon loss of the right to a special regime

After the end of the reporting year, a taxpayer who has violated the requirements for agricultural producers is obliged to recalculate tax payments.

Instead of the unified agricultural tax paid during the year, an organization or individual entrepreneur will have to calculate and pay the main types of taxes to the budget:

- property tax (if there are fixed assets);

- VAT;

- income tax (NDFL);

- income tax.

All additional tax returns must be filed by January 31, and all budget obligations must be paid during this period.

Simultaneously with the formation and submission of declarations to the Federal Tax Service under the general taxation system, the former agricultural producer is obliged to draw up an updated calculation for the Unified Agricultural Tax (advance payments) for the 1st half of the year. The amounts paid will be considered an overpayment of agricultural tax.

You can return to the use of the Unified Agricultural Tax after one year has passed after the loss of the right to use it (or voluntary refusal).

General rules and features of taxation of peasant farm activities

Unified agricultural tax = fixed interest rate * (amount of profit - amount of expenses).

Tax payments are paid at the end of the half-year and for the year. In addition, simplified accounting is used in accounting using the “cash” method. The head of the peasant farm maintains an accounting book of expenses and profits, which is not certified by the tax authorities. Rented annually:

- declaration to the Unified Agricultural Tax at the place of registration by March 31 of the following reporting year;

- Form RSV-2 (for the Pension Fund of Russia) must be submitted by March 1.

The Unified Agricultural Tax has enough advantages. A single special regime allows, for example, to write off fixed assets when they are put into operation and to include advance payments in profit. But at the same time, the head of the household will not be able to take advantage of the deferment on payments and will be required to pay land tax. Read in more detail about the use of unified agricultural tax in the article: → application of unified agricultural tax for peasant farms, payment procedure, calculation formula.

To switch to a single special regime, you must submit a corresponding application within the established time frame. Applicants can only be those from farms that are engaged in the production, sale, and processing of exclusively agricultural products with a share of this type of income of at least 70% of the total profit. Moreover, the production and sale of agricultural products in this case act as a mandatory requirement. For example, if a farm is engaged only in processing products without production, then it may be denied the transition to the Unified Agricultural Tax.

A peasant farm consisting of 3 people is engaged in the cultivation, processing and sale of vegetables and fruits. The profit of the farm is 800 thousand rubles, costs are 600 thousand rubles. Based on these data, the tax base is first calculated (based on the difference between profits and expenses): 800,000—600,000 = 200,000 rubles.

After this, the unified agricultural tax for payment to the budget is calculated. The current rate of 6% is used for calculations. The result is the following: 200,000 * 6% = 12 thousand rubles. This is the amount of single tax that will need to be paid.

| Main components of counting | Estimated data and costing |

| Data for calculation | Tax rate for Unified Agricultural Tax (6%); expenses (600 thousand rubles), profit (800 thousand rubles) |

| Tax base | Calculated using the formula: amount of profit – amount of expenses; 800000—600000=200 thousand rubles. |

| Unified agricultural tax payable | Calculation using the formula: tax base * fixed rate (6%); 200000 * 6%=12 thousand rubles. |

In order to use the unified agricultural tax, you must draw up an application in the established form and submit it to the tax office within the time limits specified by law.

The head of the peasant farm pays a single fee at the approved rate - 6.0%.

Since January 1, 2020, an innovation has appeared in the legislation, according to which individual entrepreneurs and organizations become VAT payers, in accordance with the current general procedure (clause 12 of article 9 of the Federal Law of November 27, 2017 No. 335-FZ).

The same law provides for a number of conditions that allow individual entrepreneurs and organizations working on the Unified Agricultural Tax to obtain the right to VAT exemption.

Conditions for obtaining the right not to be a value added tax payer:

If two actions were completed within one calendar year:

– transition to a special unified agricultural tax regime;

– exemption from obligations to pay VAT.

If in 2020 the peasant farm received less than 100.0 million rubles in income from its activities at the Unified Agricultural Tax

Important! For subsequent years, a limiting amount is also prescribed, which is reduced by 10 million rubles

in each subsequent annual period, so in 2021. it will amount to 70 million rubles in 2020. – 80 million rubles, for 2020 – 90 million rubles).

One-click call

The Unified Agricultural Tax has enough advantages. A single special regime allows, for example, to write off fixed assets when they are put into operation and to include advance payments in profit. But at the same time, the head of the household will not be able to take advantage of the deferment on payments and will be required to pay land tax. Read in more detail about the use of unified agricultural tax in the article: → application of unified agricultural tax for peasant farms, payment procedure, calculation formula.

Who has the right to apply the Unified Agricultural Tax?

The use of unified agricultural tax is on a voluntary basis. But it is still necessary that a mandatory condition be met - the subject must have the status of an agricultural producer. These include:

- Manufacturers of agricultural products.

- Entities engaged in primary and industrial processing of goods for the purpose of their subsequent sale.

The share of agricultural products should not be lower than 70% in relation to the total sales volume.

Persons engaged in the production of excisable goods, belonging to state or budgetary entities, are not considered payers of the Unified Agricultural Tax. If the deadline for submitting a notification is violated, the use of the unified agricultural tax may be denied.

| Contents: 1. Maintaining the accounting policy of the unified agricultural tax at the enterprise 2. Maintaining a book of income and expenses under the unified agricultural tax for individual entrepreneurs and organizations 3. Conditions for using the unified agricultural tax + infographics, calculation 4. Step-by-step instructions for registering private household plots 5. Taxation of peasant farms: comparison of the OSNO, simplified tax system, unified agricultural tax regimes 6. How to switch to the Unified Agricultural Tax from the general regime and the simplified tax system? Infographics 7. How to register a peasant farm: step-by-step instructions 8. Application of the Unified Agricultural Tax for peasant farms: infographics, calculation example, payment deadlines |

Unified agricultural tax for peasant farms

These are: In the Federal Tax Service, personal income tax declarations for their employees: 2-personal income tax for each employee until April 1; 6-NDFL for everyone quarterly within 30 days after the end of the quarter and annual form until April 1. Once a year, before January 20, information on the average number of employees is submitted to the Federal Tax Service; Payment of insurance premiums is made within 30 days after the reporting quarter, also to the Federal Tax Service.

In the Pension Fund: SZV-M until the 15th of every month; SZV-experience, EDV-1 – once a year until March 1. 4-FSS for contributions for injuries, submitted to the Social Insurance Fund by the 20th day after the reporting quarter (for electronic reporting, the deadline is until the 25th day). Can the reporting of individual entrepreneur KFC be zero? Article 346.3 states that a newly registered individual entrepreneur retains the right to apply the Unified Agricultural Tax regime if he had no income in the first tax period.

In simple words, you can take the zero grade only once. There is no need for the Federal Tax Service. 4) 2 personal income taxes until April 1 of the next year (once a year). 5) 6-NDFL is provided quarterly (no later than 1st quarter - 30.04; 2nd quarter - 31.07; 3rd quarter - 31.10; 4th quarter - 01.04). 6) ESSS (Unified Social Insurance Tax) - quarterly (no later than 1st quarter - 30.04; 2nd quarter - 31.07; 3rd quarter - 31.10; 4th quarter - 30.01) After concluding an agreement with the first hired employee, the head of the peasant farm must register in extra-budgetary funds (to the Pension Fund of the Russian Federation - within 30 days, to the Social Insurance Fund - within 10 days) Reporting to the Pension Fund of the Russian Federation (PFR): 1) SZV-M - information about insured persons monthly until the 15th day 2) Information about the length of service - SZV-M experience - once a year until March 1 For peasant farms and individual entrepreneurs using the Unified Agricultural Tax, reduced rates of insurance contributions are provided for payments and other remuneration in favor of individuals (27.1% of wages).

Attention

For some peasant farms, income tax can be reduced to zero. The full list of preferential areas is reflected in Article 284 of the Tax Code.

Income from activities not related to agriculture and farming is taxed without special benefits. Government subsidies and grants are not taxed.

The VAT return is submitted to the tax office once a quarter (in January, April, July and October before the 25th). Every year until April 30, forms 3-NDFL and 4-NDFL are provided.

These requirements apply to both individual entrepreneurs and LLCs. Form 3-NDFL must be submitted even if there was no profit.

Nuances of changing tax regimes

Organizational aspects. Let's start with the fact that organizations that have switched to paying the Unified Agricultural Tax do not have the right to switch to other taxation regimes (clause 3 of Article 346.3 of the Tax Code of the Russian Federation) before the end of the year, in particular to the traditional tax payment system. But in the course of its activities, a manufacturer may lose its status as a payer of the Unified Agricultural Tax, for example, if the share of income from sales in the total income from the sale of goods (works, services) has decreased to a level below 70%:

- agricultural products produced by the taxpayer, including primary processed products from agricultural raw materials of own production;

- agricultural products of own production, including primary processed products from agricultural raw materials.

Also, the share of agricultural income may decrease as a result of the sale of expensive fixed assets (after all, this operation is not directly related to the sale of agricultural products).

In any of the above cases, the organization loses the right to apply the special regime as a result of a decrease in the share of income from the sale of agricultural products. In this case, this right is lost no earlier than at the end of the tax period (clause 4 of Article 346.3 of the Tax Code of the Russian Federation). Then, within 15 days, the taxpayer is obliged to inform the tax authority about the transition to a different tax regime (clause 5 of Article 346.3 of the Tax Code of the Russian Federation).

Principles of changing taxation. In connection with the transition, the taxpayer should recalculate obligations for all taxes paid under the general regime. In this case, only taxes are charged. As for penalties and fines for late payment of “traditional” taxes and advance payments, penalties and fines are not paid for them (clause 4 of Article 346.3 of the Tax Code of the Russian Federation).

A taxpayer who has lost the right to use the unified agricultural tax, within one month after the expiration of the tax period in which the violation was committed, must calculate and pay VAT, corporate income tax, personal income tax, unified social tax, and corporate property tax for the entire tax period , applying the procedure for calculating “traditional” taxes provided for by tax legislation for newly created organizations or newly registered individual entrepreneurs.

The share of income from the sale of agricultural products in the total income from the sale of products (works, services) is determined only for the tax period - a calendar year. Accordingly, the recalculation of tax liabilities should be made only at the end of the tax period - the calendar year in which the organization was paying the Unified Agricultural Tax (Letter of the Federal Tax Service of Russia dated 05.08.2008 N MM-9-3/95).

For example , from January 1, 2009, an organization switched to paying unified agricultural tax. A decrease in the share of income from the sale of agricultural products in the total income from the sale of products (work, services) is planned from August 2009. If, as of December 31, 2009, income from the sale of agricultural products in the total income from the sale of goods (work, services) for 2009 is less than 70%, then the taxpayer is considered to have lost the right to apply the Unified Agricultural Tax (attention) from January 1, 2009. It turns out that the organization lost the right to use the Unified Agricultural Tax only at the end of the year, and it is considered to have switched to the general regime from the beginning this year.

Payment of the relevant taxes to the budget and submission of tax returns (according to the general regime) must be made during January 2010. If these payments are not paid by February 1, from the specified date in accordance with Art. 75 of the Tax Code of the Russian Federation, penalties will be charged for each calendar day of delay in fulfilling the obligation to pay taxes. Moreover, if the taxpayer loses the right to use the unified agricultural tax based on the results of 2009, he must submit an updated tax return for the reporting period for this tax to add up the previously accrued advance payments for it. Such recommendations are contained in the Letter of the Federal Tax Service of Russia dated January 15, 2009 N BE-22-3/ [email protected]

Specifics of applied taxation and reporting systems for peasant farms

The activities of a farm and its taxation are regulated in Russia by the Tax Code, as well as Federal Law No. 74 “On Peasant Farming” dated June 11, 2003, as amended in 2020. When submitting documents for registration of a farm, the head of the peasant farm can immediately declare the taxation regime (see →). The peasant farm (as an entrepreneur) has the right to work according to one of the systems to choose from:

- OSNO;

- Unified Agricultural Sciences.

In this case, from the moment of registration the selected taxation regime will come into force. By default, peasant farms switch to OSNO. If a month has passed after registration, if the peasant farm does not declare a transition to the unified agricultural tax or simplified tax system, the farm will be able to switch to one of these regimes only from next year. He will need to submit the application to the tax authorities by December 31.

It should be taken into account that, according to the law, peasant farms calculate, in addition to taxes, insurance contributions (to the Pension Fund of the Russian Federation, Social Insurance Fund, Federal Compulsory Medical Insurance Fund) regardless of the special regime applied. Since the participants of peasant farms are not only members of the farm, but also hired workers, the head of the farm (IP) transfers fixed insurance payments for himself and the members of the farm and at the same time pays for compulsory insurance for all employees. The procedure for payment of contributions for heads of farms is determined by Federal Law 212 of July 24, 2009, Article 14

If hired workers work in a peasant farm, under any special regime it is necessary to submit the following reports.

| Reporting forms | Due dates | Who to submit reports to? |

| 2-NDFL (on employee income); 6-NDFL (information about deductions made by the tax agent for all employees); KND 1110018 (information on the average number of employees) | Annually until 01.04; quarterly (in the current year: until May 4, August 1, October 31, annually - together with form 2-NDFL until 04/01/2017); annually: for farms created during the year - until the 20th day of the month following the one in which they were created, newly registered payers do not submit this information in the year of opening | Tax Service |

| Personalized accounting and form RSV-1; SEV-M (data on insured workers) | Quarterly (submitted on paper if there are up to 25 employees, in 2020: until May 16, August 15, November 15, for a year - until February 15, 2017); monthly (until the 10th) | Pension Fund |

| Information confirming the main activity; | Annually (until April 15); quarterly: on paper if the number of employees is up to 25, submitted before the 20th day of the month following the reporting period, in other cases, the electronic version is submitted until the 25th after the reporting period | FSS |

Start of work on Unified Agricultural Tax

Individual entrepreneurs and firms operating under a general or simplified taxation system switch to the Unified Agricultural Tax starting on January 1 of the year following the year in which the notification was submitted. Those who received the status of an individual entrepreneur or a legal entity and immediately declared their intention to apply the Unified Agricultural Tax, use this regime from the beginning of production activities.

When the right to use the unified agricultural tax is lost

Loss of the status of an agricultural producer and, accordingly, the right to apply a preferential agricultural special regime is possible in the following cases:

- reducing the mandatory 70% barrier to the share of sold agricultural products in gross income;

- violation of requirements for agricultural producers entitled to apply a special regime;

- termination of activities that give the right to apply the Unified Agricultural Tax;

- transition to another form of taxation.

Since the tax period for agricultural tax is a calendar year, all decisions regarding the loss of the right to use the Unified Agricultural Tax are made after December 31. If you refuse to further apply the special regime (regardless of the circumstances), the business entity is obliged to notify the fiscal service about this as follows:

- in case of violation of the criteria of the Unified Agricultural Tax payer - by submitting an application for loss of the right to a special tax in form No. 26.1-2;

- if you wish to use a general or simplified taxation system - according to form No. 26.1-3;

- when interrupting activities related to agriculture - according to form No. 26.1-7.

Information on the given forms must be submitted to the tax authority for a limited period - from January 1 to January 15 of the new calendar year.

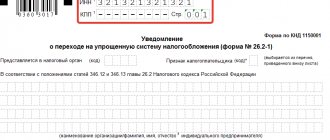

Application for transition to Unified Agricultural Tax, form 26.1-1

One of the more favorable preferential regimes for agricultural producers is the Unified National Economy. When choosing it, a business entity must know for sure that it meets the established criteria, and most importantly, the release of this product is not associated with the processing of such products. To apply this system, you need to fill out an application for transition to the Unified Agricultural Tax.

Application deadlines

The procedure for use and transition procedure are established by the Tax Code of the Russian Federation. According to these rules of law, the Unified National Economic Tax can begin to be used either from January 1 of the new year, or from the moment of registration with the Federal Tax Service.

In the first case, the business entity must send, before December 31 of the year preceding the start of application of this regime, an application, for which the order of the Federal Tax Service provides for a specific form No. 26.1-1.

The main criterion for the possibility of changing the tax system to an agricultural tax is the value of the share of revenue from the sale of agricultural products, it must be at least 70%.

Enterprises submit this form at their location, and entrepreneurs - at their registration address.

To fill out the document, you can use accounting programs or specialized Internet services. Also, organizations and individual entrepreneurs have the right to purchase a form from a printing house or print it on a computer and fill it out by hand, observing the established requirements and rules.

The application is submitted to the tax office in person, or via mail or electronic communication channel. In the first case, Form 26.1-1 can be submitted by an authorized person (individual entrepreneur or director) or a representative by power of attorney, which must be attached to the application.

An economic entity has the right to change the Unified National Economic Economy regime to another regime only at the end of the current year; to do this, it must submit a corresponding application before January 15 of the next year.

Application for closing an individual entrepreneur, form P26001

On the right is the required attribute of the applicant:

- “1” – if the document is submitted when registering a company or individual entrepreneur.

- “2” – if the document is submitted by a re-established company or entrepreneur within 30 days from the fact of registration.

- “3” – when switching from another tax system.

Then enter your full name. entrepreneur or company name. All empty cells in this block should be marked “-”.

The next step is to indicate at what point the transition to unified agricultural tax is being made. Two codes are used for this:

- “1” – from January 1, and you need to indicate from which year (Code “1” can be used by those applicants who previously indicated the sign “3”).

- “2” – from the date of registration with the tax service (new and newly opened taxpayers use code “2”.) Code “1” can be used by those applicants who previously indicated the attribute.

- “3” – transition from another system.

All empty cells are marked with a “-”.

Individual entrepreneurs and companies that previously indicated the sign “3” must enter below the percentage of income from sales of agricultural products, as well as at what point this share is calculated: “1” - based on the results of the previous year, if a transition is made from another regime; “2” – based on the results of the last reporting period for taxpayers engaged in fishing and wishing to switch from January 1 of the next year; “3” – for entrepreneurs until October 1 of the current year, transferring from the beginning of the next year.

If the application is submitted not personally by the individual entrepreneur or the director of the company, but by a representative, you must indicate on how many sheets of documents confirming the rights are attached.

Next, the form is divided into two parts; you need to fill out everything on the left. Here it is indicated who is submitting the application: “1” – personally, “2” – by a representative, enter full name.

the submitter, his telephone number, date and signature. If the application is submitted by a representative, then the name of the document confirming the authority is indicated here.

All empty cells in this part of the form are marked with a dash.

Application form according to form 26.1-1

statements in form 26.1-1 in Excel format.

Application for the transition to Unified Agricultural Tax in Pdf format.

filling out form 26.1-1 in Excel format.

Transition to OSNO

For organizations that, after the transition to a general taxation system, will use the cash method of calculating income tax, a special procedure for generating income and expenses is not provided. Therefore, for them, if the tax regime is changed, nothing will fundamentally change.

Special rules for the formation of the tax base of the transition period are established only for organizations that will determine income and expenses on an accrual basis. This follows from the provisions of paragraph 7 of Article 346.6 of the Tax Code of the Russian Federation.

Such organizations must include in the “transitional” income the amount of receivables from customers accumulated during the application of the Unified Agricultural Tax. This is explained by the fact that the unified agricultural tax system uses the cash method of income recognition. With it, income is generated as payment is received, regardless of the date of sale of goods (work, services, property rights) on account of which it was received (clause 5 of Article 346.5 of the Tax Code of the Russian Federation). Consequently, during the period when the organization applied the unified agricultural tax, the cost of goods (work, services) shipped but not paid for by buyers was not taken into account for tax purposes.

With the accrual method, a different procedure applies. Revenue is included in income as it is shipped (Clause 1, Article 271 of the Tax Code of the Russian Federation). In this regard, after the transition from the Unified Agricultural Tax to the accrual method, the cost of shipped but unpaid goods (work, services) should be reflected in income. Regardless of when the receivables are repaid, income must be increased in the month in which the organization switched to the general taxation system (clause 7.1 of Article 346.6 of the Tax Code of the Russian Federation).

If, during the period of application of the Unified Agricultural Tax, an organization received an advance, and the shipment against this advance occurred after the transition to OSNO, the amount of advances received does not need to be taken into account when calculating income tax: they should have been included in income before the transition to OSNO (clause 5 of Article 346.5 Tax Code of the Russian Federation).

As part of the “transitional” expenses, the organization that applied the Unified Agricultural Tax must include the amounts of outstanding accounts payable to suppliers, the budget, employees, etc. For example, if goods were received before the transition to the general taxation system, and paid after it, their cost must be taken into account when calculating the tax base for income tax. And if during the period of application of the Unified Agricultural Tax, goods were both purchased and paid for, after the transition to OSNO, they do not need to be included in expenses. You also do not need to take into account when calculating income tax:

– the value of the balances of finished products that existed on the date of transition to OSNO, but were sold after the transition to this taxation regime;

– the cost of raw materials and materials purchased and paid for during the period of application of the Unified Agricultural Tax, but written off for production after the transition to OSNO.

But the costs of repaying arrears of wages, insurance premiums and taxes, which arose during the period of application of the Unified Agricultural Tax, but were repaid after the transition to OSNO, should be taken into account when calculating income tax.

This is explained by the fact that the Unified Agricultural Tax uses the cash method of recognizing expenses. With it, expenses are formed as they are paid (clause 5 of Article 346.5 of the Tax Code of the Russian Federation).

With the accrual method, expenses are taken into account on the date of their implementation (clause 1 of Article 272 of the Tax Code of the Russian Federation). The date of payment does not affect the date of recognition of expenses. Regardless of when accounts payable are actually repaid, expenses must be increased in the month in which the organization switched to the general taxation system. This procedure is provided for in paragraphs 7, 7.1 of Article 346.6 of the Tax Code of the Russian Federation.

Similar clarifications are contained in letters of the Ministry of Finance of Russia dated March 21, 2014 No. 03-11-06/3/12317, dated November 11, 2013 No. 03-11-06/1/47933.

An example of accounting for receivables and payables that arose during the period of application of the Unified Agricultural Tax during the transition to a general taxation system. After the transition, the organization determines income and expenses using the accrual method

In 2014, CJSC Alfa used the Unified Agricultural Tax. In December 2014, Alpha received from a supplier a batch of raw materials for the production of products worth 100,000 rubles. In the same month, Alpha shipped products made from the raw materials received to the buyer in the amount of 130,000 rubles.

Payment for the products from the buyer was received into Alpha's bank account in February 2020. Alfa paid off its accounts payable to the supplier in March 2020.

From January 1, 2020, the organization voluntarily switched to a general taxation system using the accrual method. Alpha pays income tax on a monthly basis based on actual profits.

Alpha's accountant included the cost of received and consumed raw materials as expenses that reduce taxable profit. When calculating income tax for January 2015, the accountant took into account:

– as part of expenses – accounts payable of Alpha (RUB 100,000); – as part of income – buyer’s receivables (RUB 130,000).

If, after the transition from the Unified Agricultural Tax to the general taxation regime, an organization is recognized as a VAT payer, then the amounts of VAT presented to the organization when purchasing goods (work, services) during the period of application of the Unified Agricultural Tax are not subject to deduction (paragraph 2, clause 8, Article 346.3 of the Tax Code of the Russian Federation).

Situation: how to take into account advances issued during the period of application of the Unified Agricultural Tax, if goods (work, services) against these advances were taken into account after the transition to the general taxation system?

When calculating the Unified Agricultural Tax, advances issued are not taken into account. In order to include expenses in the calculation of the tax base, in addition to the actual payment of expenses, a counter termination of obligations is required. Therefore, before receiving goods (performing work, providing services), the amount of preliminary payments does not reduce the tax base under the Unified Agricultural Tax. This procedure follows from subparagraph 2 of paragraph 5 of Article 346.5 of the Tax Code of the Russian Federation.

The procedure for accounting for expenses prepaid before the transition to the general taxation system depends on how the organization calculates income tax: accrual or cash basis.

With the accrual method, expenses are taken into account in the period in which they arise (Clause 1, Article 272 of the Tax Code of the Russian Federation). The date of payment does not affect the date of recognition of expenses. In this regard, the cost of goods (work, services) paid before, but accepted for accounting after the transition to the general taxation system, is included in expenses when calculating income tax.

Under the cash method, expenses are recognized in the same manner as under the Unified Agricultural Tax (Clause 3, Article 273 of the Tax Code of the Russian Federation). Therefore, as counter obligations of suppliers are repaid, the cost of goods (work, services) received from them will also reduce taxable profit. But for this, the organization needs to have documents (payment orders, contracts, invoices) confirming that it paid for goods (work, services) under a transaction concluded during the period of application of the Unified Agricultural Tax. These documents will help prove that the cost of paid but not received goods (work, services) was not taken into account when calculating the unified agricultural tax and should reduce the tax base for income tax.

Regardless of the method by which the organization calculates income tax, when writing off the cost of raw materials, materials and purchased goods, comply with the conditions established by paragraph 2 of Article 272, subparagraphs 1 and 2 of paragraph 3 of Article 273, as well as Article 320 of the Tax Code of the Russian Federation.

Application for Unified Agricultural Tax when creating a peasant farm

Unified Agricultural Tax (USAT), Special tax regime for You need to pay it as when registering an individual entrepreneur - in the amount of rubles for personal To create and send an application electronically, you need. Official Internet portal of public services, city.

The general taxation system provides for the following taxes and duties to be paid by an individual entrepreneur: As can be seen from the above, most taxes and fees are associated with doing business in certain areas. Therefore, many peasant farms pay only some of the listed types of taxes: personal income tax and value added tax.

What to pay If the participants of the farm have decided to register an organization, then it becomes possible to use one of the following systems: General Taxpayer When you are on the OSSN, you must pay property, land and transport taxes, if necessary, value added tax, personal income tax as a tax agent. The mentioned benefit can be found in paragraph. Explanations are also available for personal income tax payments. For five years from the moment of registration of the farm, its members, including the head, are released from these obligations.

This benefit will remain in the event that during this time he switches to the taxation regime in the form of paying the unified agricultural tax, and then returns to the general regime of Lagutin L.

Unified agricultural tax can be used by organizations and individual entrepreneurs that are recognized as agricultural producers in accordance with Chapter. We talked in more detail about what the unified agricultural tax is and how it is calculated in a separate consultation. What is meant by peasant farm? Peasant farms are an association of citizens related by kinship or affinity, have property in common ownership and jointly carry out production and other economic activities - production, processing, storage, transportation and sale of agricultural products, based on their personal participation. Peasant farms can even consist of one person p. If a peasant farm is created by citizens, they enter into an appropriate agreement among themselves p. The peasant farm operates without forming a legal entity.

Unified agricultural tax Last updated: Only organizations and individual entrepreneurs that are agricultural producers can be transferred to pay the unified agricultural tax Unified Agricultural Tax. Agricultural producers Agricultural producers are organizations that meet the criteria given in the article

VIDEO ON THE TOPIC: Simplified taxation, imputation and patent, how to choose a tax system

When should the tax regime be changed?

Income tax. When an organization switches to paying income tax, it must be borne in mind that, in accordance with Art. Art. 285, 287 and 289 of the Tax Code of the Russian Federation, the tax calculated for the tax period (calendar year) is paid no later than March 28 of the year following the expired tax period. Advance payments based on the results of reporting periods are paid no later than 28 calendar days from the end of the reporting period.

If a taxpayer has lost the right to apply the unified agricultural tax based on the results of 2009, then he must submit tax returns on corporate income tax for the first quarter, half a year and nine months before February 1, 2010. Before the specified deadline, you also need to pay the amount of the calculated advance payment for nine months of 2009 and the monthly advance payments of the fourth quarter of 2009. Accordingly, the tax calculated for the tax period (2009) is paid no later than March 28, 2010.

Let us note that if the organization voluntarily refuses to apply the special regime, it has the right to expect to pay income tax at a zero rate, which is provided for in Art. 2.1 of the Federal Law of 06.08.2001 N 110-FZ, from January 1, 2008 to December 31, 2014 (Letter of the Ministry of Finance of Russia dated 06.22.2009 N 03-11-06/1/23). For an organization that switches to the general tax regime involuntarily due to non-compliance with the established conditions, such a conclusion is not contained in the explanation, so the taxpayer will have to pay income tax using the traditional rate.

Value added tax. Organizations that have lost the right to apply a special regime for agricultural producers from the beginning of the calendar year in which this regime was applied recalculate their VAT obligations based on the norms of the general taxation regime. It is necessary to highlight separately the calculation and acceptance of tax for deduction.

As for the accrual, the cost of goods sold (work, services) during the period of application of the special regime for agricultural producers by an organization that has lost the right to apply this regime must be increased by the corresponding tax rate (10% or 18%). The amount of revenue both from the sale of agricultural products and from other activities for the purpose of calculating VAT should be understood as:

- the amount of goods (work, services) shipped (performed, rendered) transferred during the period of loss of the right to apply the special regime, regardless of payment;

- the amount of prepayment received during the period of application of the Unified Agricultural Tax for the upcoming shipment of goods (performance of work, provision of services), transfer of property rights.

In terms of VAT deduction, the manufacturer needs to take into account the norms of clause 8 of Art. 346.3 Tax Code of the Russian Federation. Organizations that have switched from paying the Unified Agricultural Tax to a different taxation regime are recognized as VAT payers, and the tax amounts presented to them for goods (work, services), including fixed assets and intangible assets acquired before the transition to a different taxation regime, are not subject to tax deduction. Note that there is an inconsistency in this norm: on the one hand, organizations are recognized as taxpayers, on the other hand, they cannot use their right as payers to tax deductions. Tax authorities also agree with this, believing that an organization can take advantage of a tax deduction from the beginning of the year when it began to recalculate its tax liabilities (Letter of the Federal Tax Service of Russia dated January 15, 2009 N BE-22-3 / [email protected] ). There are court decisions that confirm the right of an organization to recalculate tax liabilities for the entire period of unreasonable use of the Unified Agricultural Tax using general rules governing the payment of VAT, including applying a VAT tax deduction in accordance with Art. 171 Tax Code of the Russian Federation.

Resolution of the Federal Antimonopoly Service of North Caucasus of October 18, 2006 N F08-4943/2006-2087A.

Summarize. For the entire past year, for which obligations to the budget are recalculated, the organization accrues VAT in the general manner and reduces it by the tax amounts previously taken into account in the Unified Agricultural Tax in the cost of purchased goods (works, services).

According to the Ministry of Finance (Letter dated June 15, 2009 N 03-11-06/1/22), VAT is paid either from the profits remaining after paying corporate income tax, or from the funds of buyers of goods (works, services), including number of fixed assets (in case of additional payment of the tax amount made by them). The value added tax calculated in January for the three tax periods of the previous year (I - III quarters) is paid to the budget in January of this year (until January 31 inclusive). And the calculated VAT for the tax period - the fourth quarter of the previous year is paid to the budget in accordance with clause 1 of Art. 174 of the Tax Code of the Russian Federation in equal shares no later than the 20th day of each of the three months following the expired tax period.

A few words about invoices. Organizations that pay the Unified Agricultural Tax do not issue invoices when selling goods (works, services) and property rights.

A taxpayer who has switched to the general VAT regime due to failure to comply with the conditions for paying the unified agricultural tax also does not have the right to issue invoices to customers for goods shipped last year. An exception is the case when the five-day period for issuing invoices for goods shipped, work performed, services rendered last year expires in the coming year. Then the manufacturer can issue an invoice to buyers, according to which they can deduct the tax.

Unified social tax and contributions to extra-budgetary funds. When switching to the general taxation regime, you need to know that unified social tax rates are applied to payments accrued on an accrual basis from the beginning of the year, taking into account the right to apply regression. If a taxpayer making payments to individuals during or at the end of the tax (reporting) period loses the right to use the Unified Agricultural Tax, then for the purposes of calculating the Unified Tax, he is not recognized as an agricultural producer from the beginning of 2009 and must make advance payments under the Unified Tax and submit it to the inspectorate calculations of advance payments under the Unified Social Tax for all reporting periods that have expired since the beginning of the year.

Let us recall that the organization reduces the amount of unified social tax transferred to the federal budget by the amount of contributions for compulsory pension insurance, which are paid when applying any taxation regime, taking into account the application of regressive tax rates. Therefore, the change in the tax regime will not affect the procedure for paying contributions to compulsory pension insurance. The same can be said about contributions for insurance against industrial accidents and occupational diseases; they do not need to be recalculated due to a change in the taxation regime.

Property tax. If an organization has lost the right to apply the unified agricultural tax based on the results of 2009, it must recalculate the corporate property tax for the entire 2009. More precisely, accrue and then pay the property tax for the entire 2009 by February next year, not forgetting to submit tax returns to the inspectorate regarding the amounts paid.

Taxation of peasant farming, special regimes and reporting

Many peasant farms remain on the general taxation system in order to retain customers for their products, since most wholesale buyers work for OSNO and in order to reduce their tax burden they simply need to purchase products from organizations (individual entrepreneurs, peasant farms) that work with VAT, since only in this case they will be able to reimburse the VAT paid for the products from the budget. Insurance premiums are differentiated for members of peasant farms and for employees.

Info

For members of peasant farms there are fixed rates, calculated on the basis of the minimum wage, relevant for individual entrepreneurs. The simplified taxation system for KFC is traditional.

Who benefits from using OSNO

Despite the complexity of keeping records, calculating and paying several types of taxes and the significant amount of reporting submitted, the traditional taxation system is the most profitable for the following business entities:

- Individual entrepreneurs and organizations engaged in wholesale trade.

The use of special regimes when conducting wholesale trade is impossible in most cases, since this type of activity does not fall under UTII and PSN, and there is a limit on the simplified tax system, exceeding which deprives an individual entrepreneur or organization of the right to apply this taxation regime (in 2020 it is 150 million). rub.).

- Individual entrepreneurs and organizations whose counterparties are interested in “input” VAT.

If most of the contractors of individual entrepreneurs and organizations use OSNO and are interested in offsetting the “input” VAT, the best option would be to use OSNO, since the OSNO tax paid to the seller (counterparty) can be claimed as a deduction.

Note: if an individual entrepreneur or organization is not a VAT payer (applies a special tax regime), it cannot claim this tax as a deduction (reduce), and therefore VAT is either included in the cost of the product, which significantly increases its price, or is paid from its own funds, which in the first case is not beneficial to buyers who pay VAT, and in the second case it is not beneficial to the seller, since he is obliged to pay the VAT received from the buyer according to the invoice to the budget.

- Individual entrepreneurs and organizations importing goods into Russia.

Importers benefit from this taxation regime, since the VAT paid upon import into the territory of the Russian Federation can subsequently be claimed as a deduction.

- Individual entrepreneurs and organizations with VAT and income tax benefits.

Specifics and advantages of possible taxation regimes for peasant farms in comparison

The choice of special regime depends largely on the main indicators of the farm’s agricultural activity, primarily on the amount of profit, size and volume of products produced. One should proceed from the specifics of the operation of the farm itself and the taxation that suits it best.

The significant difference between the three systems is visible primarily in the tax burden and associated restrictions, which should be taken into account when deciding on the use of special regimes. It should also be noted when comparing the fact that the composition of the calculated taxes of peasant farms and individual entrepreneurs is mostly identical.

| Special modes | BASIC | USN (Profit): | USN (Profit-Expense) | Unified agricultural tax |

| Basic tax payments and rates | Personal income tax (13% for residents, 30% for non-residents of the Russian Federation), VAT (10 or 18%), property, transport and land taxes | Single profit tax at a rate of 6% | A single tax at a rate of 5-15% on the difference between profit and expense (if costs exceeded profit, then 1% of annual profit) | Unified agricultural tax at a rate of 6%; 0% for Crimea and Sevastopol in 2020 and 4% in subsequent years until 2021; transport and land taxes |

| Restrictions on use | — | yes (Tax Code of the Russian Federation, Art. 346.12 and 346.13) | yes (Tax Code of the Russian Federation, Art. 346.12 and 346.13) | yes (Tax Code of the Russian Federation, Art. 346.2, clause 2 and clause 5) |

| Restrictions on type of activity | — | — | — | yes (Tax Code of the Russian Federation, Art. 346.2, clause 2) |

The general taxation procedure provides a wide range of opportunities for developing a serious business. Among the obvious advantages are the possibility of VAT reimbursement, taking into account costs and damages in tax calculations, and the absence of any restrictions. The simplified tax system significantly reduces the tax burden, which will most likely attract newcomers to entrepreneurship. Well, the Unified Agricultural Tax is designed specifically for workers in the agro-industrial complex, taking into account the specifics of their work.

Let's sum it up

Farmers have the right to choose one of three possible special regimes. They cannot be combined.

The Unified Agricultural Tax is intended for a narrow circle of agricultural producers with a profit of at least 70% of the total income. It is for them that a low rate, simplified accounting, and favorable payment terms are provided.

The simplified tax system is more often used when the number of employees is up to 100 people and the annual profit exceeds 45 million rubles. The simplified tax system (Profit) is suitable for a farm whose profit exceeds expenses, and the simplified tax system (Profit-Expense) is suitable for activities with high production costs.

One-click call