Deadlines for submitting reports to the Federal Tax Service in 2020

The table below indicates the deadlines for submitting the main reports submitted to the Federal Tax Service (including new reports), taking into account postponements for all companies and individual entrepreneurs due to coronavirus, quarantine and non-working days in 2020.

Table. Deadlines for submitting reports to the tax office

| Reporting type | Period | Deadline for sending to the Federal Tax Service |

| Certificates 2-NDFL | For 2020 | No later than 03/02/2020 |

| For 2020 | No later than 03/01/2021 | |

| Calculation of 6-NDFL | For 2020 | No later than 03/02/2020 Transfer to 06/01/2020 |

| For the first quarter of 2020 | No later than 04/30/2020 Transfer to 07/30/2020 | |

| For the first half of 2020 | No later than 07/31/2020 | |

| For 9 months of 2020 | No later than 02.11.2020 | |

| For 2020 | No later than 03/01/2021 | |

| Calculation of insurance premiums (ERSV) | For 2020 | No later than 01/30/2020 |

| For the first quarter of 2020 | No later than 04/30/2020 Transfer to 05/15/2020 | |

| For the first half of 2020 | No later than 07/30/2020 | |

| For 9 months of 2020 | No later than 10/30/2020 | |

| For 2020 | No later than 02/01/2021 | |

| Information on the average number of employees | For 2020 | No later than 01/20/2020 |

| For 2020 | No later than 01/20/2021 | |

| Income tax return (for quarterly reporting) | For 2020 | No later than 03/30/2020 Transfer to 06/39/2020 |

| For the first quarter of 2020 | No later than 04/28/2020 Transfer to 07/28/2020 | |

| For the first half of 2020 | No later than July 28, 2020 | |

| For 9 months of 2020 | No later than October 28, 2020 | |

| For 2020 | No later than March 29, 2021 | |

| Income tax return (for monthly reporting) | For 2020 | No later than 03/30/2020 Transfer to 06/29/2020 |

| For January 2020 | No later than 02/28/2020 | |

| For January – February 2020 | No later than 03/30/2020 Transfer to 06/29/2020 | |

| For January – March 2020 | No later than 04/28/2020 Transfer to 07/28/2020 | |

| For January – April 2020 | No later than 05/28/2020 Transfer to 08/28/2020 | |

| For January – May 2020 | No later than 06/29/2020 | |

| For January – June 2020 | No later than July 28, 2020 | |

| For January – July 2020 | No later than 08/28/2020 | |

| For January – August 2020 | No later than September 28, 2020 | |

| For January – September 2020 | No later than October 28, 2020 | |

| For January – October 2020 | No later than November 30, 2020 | |

| For January – November 2020 | No later than 12/28/2020 | |

| For 2020 | No later than March 29, 2021 | |

| VAT declaration | For the fourth quarter of 2020 | No later than 01/27/2020 |

| For the first quarter of 2020 | No later than 04/27/2020 Transfer to 05/15/2020 | |

| For the second quarter of 2020 | No later than July 27, 2020 | |

| For the third quarter of 2020 | No later than October 26, 2020 | |

| For the fourth quarter of 2020 | No later than 01/25/2021 | |

| Journal of received and issued invoices | For the fourth quarter of 2020 | No later than 01/20/2020 |

| For the first quarter of 2020 | No later than 04/20/2020 Transfer to 05/06/2020 (if the company did not operate on non-working days) | |

| For the second quarter of 2020 | No later than July 20, 2020 | |

| For the third quarter of 2020 | No later than October 20, 2020 | |

| For the fourth quarter of 2020 | No later than 01/20/2021 | |

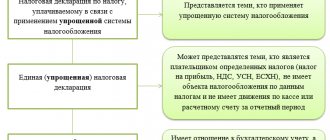

| Tax declaration under the simplified tax system | For 2020 (represented by organizations) | No later than 03/31/2020 Transfer to 06/30/2020 |

| For 2020 (represented by individual entrepreneurs) | No later than 04/30/2020 Transfer to 07/30/2020 | |

| For 2020 (represented by organizations) | No later than 03/31/2021 | |

| For 2020 (represented by individual entrepreneurs) | No later than 04/30/2021 | |

| Declaration on UTII | For the fourth quarter of 2020 | No later than 01/20/2020 |

| For the first quarter of 2020 | No later than 04/20/2020 Transfer to 07/20/2020 | |

| For the second quarter of 2020 | No later than July 20, 2020 | |

| For the third quarter of 2020 | No later than October 20, 2020 | |

| For the fourth quarter of 2020 | No later than 01/20/2021 | |

| Declaration on Unified Agricultural Tax | For 2020 | No later than 03/31/2020 Transfer to 06/30/2020 |

| For 2020 | No later than 03/31/2021 | |

| Declaration on property tax of organizations | For 2020 | No later than 03/30/2020 Transfer to 06/30/2020 |

| For 2020 | No later than 30.03.2021 | |

| Transport tax declaration (submitted only by organizations) | For 2020 | No later than 02/03/2020 |

| Land tax declaration (submitted only by organizations) | For 2020 | No later than 02/03/2020 |

| Single simplified declaration | For 2020 | No later than 01/20/2020 |

| For the first quarter of 2020 | No later than 04/20/2020 Transfer to 07/20/2020 | |

| For the first half of 2020 | No later than July 20, 2020 | |

| For 9 months of 2020 | No later than October 20, 2020 | |

| For 2020 | No later than 01/20/2021 | |

| Declaration in form 3-NDFL (submit only individual entrepreneurs) | For 2020 | No later than 04/30/2020 Transfer to 07/30/2020 |

| For 2020 | No later than 04/30/2021 |

Tax reporting for individual entrepreneurs with simplification, OSN, UTII

Reporting provided for individuals can be divided into the following categories:

- reporting, depending on the use of a particular tax calculation system;

- reporting for employees, if any;

- reporting on cash transactions.

Reporting depending on the taxation system used

Based on the chosen tax calculation system, the individual entrepreneur must provide the following documents to the Federal Tax Service:

| Tax regime | Tax return | Delivery deadlines |

| Simplified tax system | simplified tax system | According to the results of the reporting year until April 30 of the current period |

| Imputed profit tax | UTII | At the end of each quarter until the 20th day of the month following it |

| General taxation system | 3-NDFL | According to the financial results of the past year until April 30 of this period |

| 4-NDFL | No later than 5 days after the end of the month in which the profit was made | |

| VAT calculation | Quarterly until the 25th day of the month following the quarter |

It is important ! In cases where several tax regimes are used at once, it is necessary to separately carry out accounting, provide reporting to the Federal Tax Service and pay taxes.

Book of accounting of expenditure transactions made and profit received

Maintaining this form is provided for all individual entrepreneurs using OSN and STS. But since 2013, it is not required to be certified by the tax office. At the same time, every entrepreneur must have a numbered and laced KUDIR; failure to do so will result in a fine of 200 rubles.

Individual entrepreneurs using UTII do not keep a book, but in this case they take into account material indicators: square meters, number of staff units. How exactly they should do this is not provided for by law.

Reporting provided for by the Tax Code of the Russian Federation for employees

It can be divided into several categories:

- Federal Tax Service reporting;

- documentation provided to the Pension Fund and Social Security.

Tax reporting provided by the organization for its employees, if any:

| Where do we rent? | What we rent | When we rent |

| Inspectorate of the Federal Tax Service | Help on form 2-NDFL | According to the results of the calendar year until April 1 of the current year |

| Average number of employees | Based on the results of the previous year until January 20 following the reporting year | |

| Calculation according to form 6-NDFL | Quarterly no later than the last day of the month following the reporting period |

Cash transactions: reporting

Individual entrepreneurs carrying out operations directly related to the issuance, storage, and registration of cash financial resources are required to adhere to cash discipline: compliance with the established limit, generation of cash documents.

Keeping records of cash transactions does not depend on the taxation system and the availability of a cash register. In the absence of a cash register, you can use forms that are strict reporting documents. Since the beginning of 2014, the implementation of cash transactions for individual entrepreneurs has been significantly simplified - there is no need to use a cash book and cash register.

Entrepreneurs generate only documents on the basis of which they can confirm the payment of wages. According to the simplified procedure, small organizations and individual entrepreneurs (number of employees no more than 100 and revenue less than 800 million per year) no longer set a cash balance limit.

Deadlines for submitting reports to the Pension Fund in 2020

The following reports must be submitted to the Pension Fund (PFR):

| Reporting type | For what period is it represented? | Deadline for submission to the Pension Fund |

| Information about insured persons in the Pension Fund (SZV-M) | For December 2020 | No later than 01/15/2020 |

| For January 2020 | No later than 02/17/2020 | |

| For February 2020 | No later than 03/16/2020 | |

| For March 2020 | No later than 04/15/2020 | |

| For April 2020 | No later than 05/15/2020 | |

| For May 2020 | No later than 06/15/2020 | |

| For June 2020 | No later than 07/15/2020 | |

| For July 2020 | No later than 08/17/2020 | |

| For August 2020 | No later than September 15, 2020 | |

| For September 2020 | No later than 10/15/2020 | |

| For October 2020 | No later than 11/16/2020 | |

| For November 2020 | No later than 12/15/2020 | |

| For December 2020 | No later than 01/15/2021 | |

| Information about the insurance experience of the insured persons (SZV-STAZH) | For 2020 | No later than 03/02/2020 |

| For 2020 | No later than 03/01/2021 | |

| Information on the policyholder transferred to the Pension Fund for maintaining individual (personalized) records (EFV-1) | For 2020 | No later than 03/02/2020 |

| For 2020 | No later than 03/01/2021 | |

| Information on the labor activity of employees (SZV-TD) | For January 2020 | No later than 02/17/2020 |

| For February 2020 | No later than 03/16/2020 | |

| For March 2020 | No later than 04/15/2020 (the issue of postponing the deadline to 05/06/2020 is controversial) | |

| For April 2020 | No later than 05/15/2020 | |

| For May 2020 | No later than 06/15/2020 | |

| For June 2020 | No later than 07/15/2020 | |

| For July 2020 | No later than 08/17/2020 | |

| For August 2020 | No later than September 15, 2020 | |

| For September 2020 | No later than 10/15/2020 | |

| For October 2020 | No later than 11/16/2020 | |

| For November 2020 | No later than 12/15/2020 | |

| For December 2020 | No later than 01/15/2021 |

BASIC

As before, the most labor-intensive reporting can be considered reporting under the general taxation system. An accountant who services companies on OSNO will have to submit more than a dozen different reports in 2020, including:

1. Tax returns for:

- VAT;

- arrived;

- property;

- transport;

- earth.

2. Reporting to extra-budgetary funds:

- 4-FSS;

- confirmation of the main type of activity;

- SZV-M;

- SZV-experience.

3. Other reporting to the Federal Tax Service:

- calculation of insurance premiums;

- information on the average number of employees;

- 2-NDFL;

- 3-NDFL;

- 6-NDFL;

- financial statements (balance sheet and appendices thereto).

Deadline for submitting reports to the Social Insurance Fund in 2020

The deadline for submitting 4-FSS depends on the method of submitting the calculation:

| Reporting type | For what period is it represented? | Deadline for submission to the FSS |

| Calculation of 4-FSS on paper | For 2020 | No later than 01/20/2020 |

| For the first quarter of 2020 | No later than 04/20/2020 Transfer to May 15, 2020 | |

| For the first half of 2020 | No later than July 20, 2020 | |

| For 9 months of 2020 | No later than October 20, 2020 | |

| For 2020 | No later than 01/20/2021 | |

| Calculation of 4-FSS in electronic form | For 2020 | No later than 01/27/2020 |

| For the first quarter of 2020 | No later than 04/27/2020 Transfer to May 15, 2020 | |

| For the first half of 2020 | No later than July 27, 2020 | |

| For 9 months of 2020 | No later than October 26, 2020 | |

| For 2020 | No later than 01/25/2021 | |

| Confirmation of main activity | For 2020 | No later than 04/15/2020 Transfer to May 6, 2020 - if the employer was subject to the non-working days regime (i.e. did not function during this period). |

| For 2020 | No later than 04/15/2021 |

Control ratios in reporting

When submitting reports to the Federal Tax Service, it is necessary to take into account that all indicators are interrelated, therefore, for each type of declarations and other reports, control relationships (intra-documentary and inter-documentary) are provided, approved at the legislative level and published in the public domain for public use, for example, on the official website of the Federal Tax Service. Control ratios must be observed even with forms that the organization develops independently. Provided that some ratios do not converge, the Federal Tax Service has the right to request clarification on the report, which must be submitted within 10 days with supporting documents attached. Therefore, before submitting reports, you need to make sure that the calculations are correct so that there are no disagreements with the tax office.

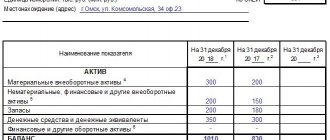

The organization's financial statements are presented by the following documents:

- Balance sheet

- Income statement

- Statement of changes in equity

- Cash flow statement

- Explanations to the balance sheet and income statement

Form 1 (balance sheet) is associated with all reporting forms.

The relationships between such forms as: 6-NDFL with 2-NDFL, DAM, income tax declaration must also be observed.

Thus, in one enterprise all reporting indicators are interconnected. Based on this, you can check the correctness of reporting before submitting it.

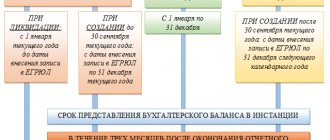

Deadline for filing financial statements in 2020

As a general rule, organizations must submit financial statements for 2020 only to the INFS. They must do this electronically. True, organizations belonging to small and medium-sized businesses can submit reports for 2020 on paper:

- Financial statements for 2020 must be submitted no later than 03/31/2020 ( postponed to 05/06/2020 ).

- financial statements for 2020 must be submitted no later than 03/31/2021.

Read also

01.05.2020 06.05.2020 07.05.2020 15.05.2020 16.07.2020 30.01.2020