How to pay wages

The employer is required to pay wages at least twice a month. Payment can be made:

- non-cash - by transferring funds to a bank card or other bank account of the employee;

- in cash through the company's cash desk.

The procedure for documenting non-cash transfers is usually regulated by an agreement concluded between the bank and the organization. In case of payment of wages through the cash register, one of three documents must be completed:

- payroll;

- payroll;

- cash order (possibly if payment is made to one employee).

If the funds in the cash register are not enough to pay salaries, then they must be received from the current account. Cash for payment of wages can be kept in the cash register for no more than five days. During this time, the employee has the right to apply to the organization’s cash desk to receive his due salary. After the expiration of the five-day period, wages not received by employees are deposited.

How to correctly fill out the T-49 payroll form?

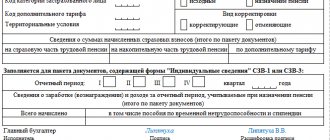

Filling out the title page of the payroll statement T-49

The following information must be filled in on the title page:

- the name of the enterprise (organization, individual entrepreneur, structural unit (if there is none, a dash is placed) and its organizational and legal form;

- OKPO;

- date of filling out the statement;

- Document Number;

- amount of funds in words and figures;

- salary payment deadline;

- month of calculation and payment of wages (reporting period);

- signature of the head of the organization;

- accountant's signature.

According to the legislation of the Russian Federation, the period for issuing funds is 5 days.

Filling out the table in the payroll statement T-49

The payroll table of Form T-49 is filled out as follows:

- serial number;

- Personnel Number;

- position (profession);

- tariff rate.

- number of days worked;

- amount of accruals (salary, advance payment, compensation for unused vacation, other income);

- personal income tax amount;

- amount of debt owed by the organization/employee;

- amount to be paid;

- surname and initials of the employee who received the money;

- or a record of deposit of the amount, if it is not received within 5 days.

All entries must match the entries in the employee’s personal card (number of hours worked, days, including working days, holidays and weekends).

The data is taken from the working time sheet.

In the last column, the “Total” columns indicate the entire amount accrued to the employee.

If the money was not received on time, the cashier marks the deposit. After recalculating the money, the employee signs the T-49 payroll form. Salary payments are made in rubles.

The number of rows in the table must correspond to the number of employees (one row for each employee).

At the end of the document (after the table) information about the issued and deposited amount of funds is entered.

After this, the document is signed by the cashier and accountant of the enterprise (with the initials deciphered), and the date and number of the cash order are also indicated.

You can fill out the document either in printed form or manually.

Which document form to use?

From 01/01/2013, organizations have the right to independently develop primary accounting documents, including those for the payment of wages. The primary documents must provide for the presence of all mandatory details in accordance with Part 2 of Art. 9 of Law No. 402-FZ.

But many companies continue to use forms approved by Goskomstat. Thus, Resolution No. 1 of January 5, 2004 approved the following forms:

- T-49 “Payment and payroll”;

- T-51 “Payment sheet”;

- T-53 “Payroll”.

If the organization uses form T-49, forms T-51 and T-53 are not drawn up. Next, we will tell you in more detail about the rules for filling out the unified form T-49 (the payroll sheet can be found at the end of the article).

Purpose of this document

The payroll form T-49 is simultaneously both a settlement and a payment document. The purpose of this statement is to simplify document management (firms, organizations, enterprises, individual entrepreneurs). Payroll T-49 allows you to fill out one document instead of several.

This is a form of primary accounting reporting. The statement is compiled on the basis of another document. It is called a time sheet (unified form T-13).

In addition, the payroll form T-49 replaces two other documents:

- Payroll form T-51.

- Payroll form T-53.

Organizations, firms, enterprises or individual entrepreneurs, in accordance with current legislation, have the right to independently determine which form of payroll statements is the most acceptable (T-49, T-51 or T-53).

Rules for filling out form T-49

Filling out the document is possible both manually and in typewritten form using appropriate software. Form T-49 “Payment Sheet” is compiled in one copy and stored in the accounting department.

Payroll is calculated separately for each employee. Information about hours worked is transferred from time sheets. Accruals are calculated based on the time worked or output of the employee. Information about accruals due is filled in based on the following data:

- employment contracts (salary, bonus for qualifications);

- provisions on wages and bonuses for employees;

- bonus orders.

After this, deductions are calculated for each employee and the amount payable is calculated. The title page indicates the total amount to be paid to all employees. The manager (or other authorized person) makes a record of the transfer of the document for making payments through the cash register.

After the deadline for the payment of wages expires, a deposit note is made opposite the names of employees who have not received wages. A summary of amounts paid and deposited is provided at the end of the document. A note is also made there about the number and date of the cash register, as well as the signatures of the cashier and the accountant who checked all the records.

Entering data

A sample for filling out a payroll slip requires an indication of the completeness of its component parts. It is worth considering each of them in more detail.

Design of the first part

Filling out the title involves entering the following parameters into it:

- legal name of the individual entrepreneur;

- TIN;

- date of data entry;

- serial number ;

- the total amount required to ensure full payment;

- time frame for payment, which by law cannot exceed 5 days;

- reporting period;

- signature of the manager;

- signature of the responsible accountant.

This part contains general information about individual entrepreneurs and the payroll.

Table design

To fill out the tabular part of the T-49 form, you must indicate the individual data of each employee, namely:

- serial number in the payroll form;

- personnel number from your personal file;

- position held;

- salary specified in the Employment Agreement;

- how long the employee actually worked,

- additional hours during non-working hours, etc.

The last column of the “Total” table involves indicating the amount of payment to the employee, taking into account all accruals and deductions.

Having received the funds, the employee puts his signature as confirmation. If the payment was not made on time, the cashier makes a note about the deposit. The number of employees of an individual entrepreneur must be equal to the number of columns, that is, one full row per staff unit.

The final part of the document should contain the total of how much funds were issued and deposited. After this, the statement is once again certified by the signature of the accountant and cashier, indicating the surname and initials. In addition, the number and date of the cash order are indicated.

If detected, it is possible to make corrections in the payroll, but without using a barcode corrector. The data correction sample requires entering the correct information with the signature of the cashier and accountant.

Sample of filling out a payroll slip

Initial data on working days, salaries and other payments of employees of LLC "Company" for August 2020:

| FULL NAME. | Days worked | Vacation, days | Salary according to employment contract | Bonus by order | Vacation pay |

| Ivanov I.I. | 23 | 50 000 | 5000 | ||

| Petrova P.P. | 23 | 30 000 | 4000 | ||

| Semenova S.S. | 13 | 10 | 20 000 | 3000 | 12 000 |

According to the schedule in August there are 23 working days. All employees pay personal income tax at a rate of 13%, there are no other deductions.

Let's fill in the document details.

We will calculate your salary and calculate the amount of tax to be withheld.

After calculating the amounts to be paid, the director of the company must make a record of transferring the statement to the cash desk for issuing funds to employees.

Having received the due salary, each employee signs next to his last name in the appropriate line.

Upon completion of the payment of the salary, at the end of the document the cashier will make a note about the amounts paid and put his signature. Since all employees received salaries, no record is made of the amounts deposited. After the check, the accountant also puts his signature confirming that all entries in the payroll sheet are correct

Let's move on to the tabular part of the payroll document

In column 1 the numbers are written in order, the last number must be equal to the number of employees on staff. Column 22 of the payroll list indicates the entire list of employees with whom employment contracts were concluded at the enterprise. Columns 2, 3, 4 of the payroll sheet are filled out based on the information from the employee’s personal card (form No. T-2). Columns 5, 6, 7 of the payroll sheet are filled out on the basis of the information specified in form No. T-13 “Ticket for recording the use of working time.” In the section “Accrued for the current month (by type of payment)” in the corresponding columns (8-13) the amount of accrual of the worker’s wages is indicated (the column and separately accruals that were received by the employee, but are not related to the performance of any duties provided for in employment contract (column 9 “Payment for business trips”, column 10 “Temporary disability benefits”, column 11 “Payment for regular vacation”, etc.) Column 14 “Total” indicates the total amount for each line, obtained by adding all the data in columns 8-13. The section “Withheld and set off” reflects the amounts that are withheld from wages (mandatory deductions and deductions at the request of the employee or at the initiative of the administration). These are columns 15-18. There may be “Income tax” (column 15 ), which is equal to 13% of the total amount of accruals (column 14), “Advance” (column 16), which is paid for the first half of the current month and other deduction amounts (loan repayment amounts, deductions under writs of execution, etc.). Column 19 of the payroll statement indicates the amount that the recipient of the funds owes to the company. Next, we calculate the following difference for each line: the sum of the numbers from columns 14 and 19 minus the sum of the numbers from columns 15-18. We record the positive difference in column 21, the negative difference in column 20. For each column, the total amount is entered in the bottom line. The total amount in column 21 is transferred to the “Amount” line. After registration, the statement is handed over to the cashier to check its correctness. If the statement is completed incorrectly, it is sent back to the accounting department. If the statement is completed correctly, the cashier can begin issuing money to employees according to it. He draws up a cash settlement for the total amount that will be paid according to the statement (lines “Cash outgoing order No.” and date of preparation). In column 23 of the payroll sheet, the employee puts his signature next to his last name if the money is paid to him. If money has not been paid to any employee, then the cashier must write “Deposited” in this column. Payments are made by a cashier or accountant (the position, signature and its decoding as surname and initials are indicated). In the line “The amount has been paid according to this payroll,” the cashier, in words and then in numbers, indicates the total amount paid to employees, respectively, in the line “and the amount deposited” the total deposited amount is indicated.

The T-49 payroll form is completed. The final stage of drawing up the payroll statement is the signature of the chief accountant and the date of its certification.

Payment and payslips T-49, T-51 and T-53 (download)

At the end of this page you can download forms of payroll T-49, payroll T-51 and payroll T-53.

Statements are used for the purpose of calculating wages for employees, as well as carrying out the procedure for paying them. Statistical authorities provided three types of such statements:

- Settlement and payment (T-49);

- Settlement (T-51);

- Payment (T-53).

Moreover, if a document is drawn up in form T-49, statements on the other two forms do not need to be drawn up. A payroll sheet is drawn up to pay salaries to employees based on information about the amount of time actually worked or products produced, and a payroll sheet is drawn up to process the payment of salaries to employees. The T-49 form combines both functions. The accountant is responsible for preparing the statement; the document is drawn up in one copy.

If employees receive their salaries using bank plastic cards, only a payslip is required. The need to prepare payroll statements arises in cases where salaries are issued to employees from the company's cash desk.

The “Accrued” field indicates the amounts by type of payment and other income that are paid from the company’s profits and are subject to inclusion in the tax base. Then all deductions are calculated and the amount to be paid is displayed.

On pay slips, the total amount payable is listed on the title page of the document. Permission to make payments to employees must be endorsed by the head of the company. At the end of the statement, after payments have been made, you must indicate the amounts of paid and deposited salaries.

A settlement account is drawn up for the issued salary amount, and its details are indicated in the statement. Opposite the names of employees who did not receive their salaries on time, the inscription “DEPOSITED” is placed.

Forms T-49 and T-53 are mandatory for use if salaries are paid in cash from the company’s cash desk - the corresponding clause is in the Directive of the Central Bank of the Russian Federation No. 3210-U dated March 11, 2014.

Download statement forms:

Download form T-49 (in XLS format, editable in Microsoft Excel)

Download form T-51 (in XLS format, editable in Microsoft Excel)

Download form T-53 (in XLS format, editable in Microsoft Excel)

Documents on the website How to earn money.ru are always relevant. Attention! If you notice an error or irrelevance of the document, please report it in the comments.