If you think that understanding tax regimes is very difficult, then you are not alone, Albert Einstein himself is in your company. The creator of the theory of relativity believed that the most incomprehensible thing in this world is the tax scale. However, if you want to conduct an effective, financially, entrepreneurial activity, you will still have to understand this.

And for those who still have questions or those who want to get advice from a professional, we can offer a free consultation on taxation from 1C specialists:

Free tax consultation

What is the tax system?

The taxation system refers to the procedure for collecting taxes, that is, those monetary contributions that each person receiving income gives to the state. Taxes are paid not only by entrepreneurs, but also by ordinary citizens whose income consists only of salaries. With proper planning, the tax burden of a businessman can be lower than the income tax of an employee.

Well, since we are talking about the taxation system, we need to understand its main elements. According to Art. 17 of the Tax Code of the Russian Federation, a tax is considered established only if the taxpayers and elements of taxation are determined, namely:

- object of taxation – profit, income or other characteristic, the appearance of which creates an obligation to pay tax;

- tax base – monetary expression of the object of taxation;

- tax period – a period of time at the end of which the tax base is determined and the amount of tax payable is calculated;

- tax rate – the amount of tax charges per unit of measurement of the tax base;

- tax calculation procedure;

- procedure and deadlines for tax payment.

Today in Russia you can work under the following tax regimes (taxation systems):

- OSNO – general taxation system;

- STS is a simplified taxation system in two different versions: STS Income and STS Income minus expenses;

- UTII – single tax on imputed income (cancelled from 2021);

- Unified agricultural tax - unified agricultural tax;

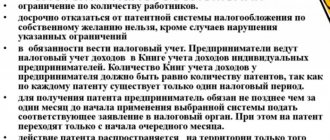

- Patent taxation system (only for individual entrepreneur taxation)

- NPA - tax on professional income (available to individual entrepreneurs and individuals without registering as an individual entrepreneur).

As you can see, there is plenty to choose from.

In our service you can prepare a notification about the transition to the simplified tax system absolutely free of charge:

Create an application for the simplified tax system for free

Note: There is another rarely used taxation system - when executing production sharing agreements , which is used in the extraction of mineral resources, but we will not consider it within the scope of this article.

Let's take a look at the main elements of Russian tax regimes. Let's take into account that several different taxes are paid on OSNO: VAT, property tax of organizations or individuals, plus individual entrepreneurs on OSNO pay income tax on individuals, and organizations pay income tax.

| Element | simplified tax system | UTII | Unified agricultural tax | PSN | BASIC |

| Object of taxation | Income (for the simplified tax system Income) or income reduced by expenses (for the simplified tax system Income minus expenses | Taxpayer's imputed income | Income reduced by expenses | Potential annual income | For income tax - profit, that is, income reduced by the amount of expenses. For personal income tax - income received by an individual. For VAT – income from the sale of goods, works, services. For property tax of organizations and individuals – real estate. |

| The tax base | The monetary expression of income (for the simplified tax system Income) or the monetary expression of income reduced by expenses (for the simplified tax system Income minus expenses) | Monetary value of imputed income | Monetary value of income reduced by expenses | Monetary value of potential annual income | For income tax - the monetary expression of profit. For personal income tax – the monetary expression of income or the value of property received in kind. For VAT – revenue from the sale of goods, works, services. For corporate property tax – the average annual value of property. For personal property tax, the inventory value of the property. |

| Taxable period | Calendar year | Quarter | Calendar year | Calendar year or period for which the patent was issued | For income tax - calendar year. For personal income tax – calendar year. For VAT – quarter. For property tax of organizations and individuals - calendar year. |

| Tax rates | by region from 1% to 6% (for the simplified tax system Income) or from 5% to 15% (for the simplified tax system Income minus expenses) | 15% of imputed income | 6% of the difference between income and expenses | 6% of potential annual income | For income tax - 20% in general, and from 0% to 30% for certain categories of payers. For personal income tax – from 13% to 30%. For VAT – 0%, 10%, 20% and calculated rates in the form of 10/110 or 20/120. For corporate property tax – up to 2.2% For personal property tax – up to 2%. |

OSNO without VAT for individual entrepreneurs

OSNO represents the general taxation system, or the main one. Several types of taxes are paid in this mode. The difficulty of working with SES is the need to prepare reports on financial activities, as a result, some individual entrepreneurs switch to preferential treatment.

There are various reasons why IPs choose the OCH mode. This is due to the fact that most large partners work with VAT, and they choose counterparties who work according to the same scheme. In addition, the regime does not provide limits on possible profits and the number of employees. Due to the specifics of their activities, not all individual entrepreneurs can apply a regime other than OSNO to work without VAT.

If you work in this mode, you must pay not only value added tax, but also personal income tax and property tax. VAT is an indirect tax and is paid by the end consumer. The basis is defined as the cost of goods sold. In total, there are three main rates for this type of fee - a general rate of 20%, preferential rates - 0 and 10%.

In some cases, an exemption from making this type of payment may apply. Its features are reflected in Article 145 of the Tax Code. The right to exemption can be used if for the three previous periods the amount of revenue is less than 2,000,000. This privilege does not apply to persons who sell excisable goods.

To obtain an exemption from making a payment, you should contact the fiscal authority at your place of registration. You must provide a pre-filled notification and extracts from the books of income and expenses. Eligibility for exemption must be verified annually. Moreover, if the revenue has become higher, the tax service must be notified about this, otherwise the fiscal authority may apply sanctions.

Not all organizations and individual entrepreneurs receive a full exemption from VAT. In this case, you can reduce the amount of deductions by using deductions. According to Article 171 of the Tax Code, payers have the right to apply for compensation. To apply for a deduction, a number of requirements must be met:

- Products purchased by the organization are accepted for accounting.

- The company has documents that confirm the right to receive compensation.

- Products or works must be purchased for use in a taxable activity.

Organizations and individual entrepreneurs can independently decide whether there is a need to work on OSNO. Many people choose the basic tax regime, as it is easier to cooperate with large companies.

What influences the ability to choose a tax system?

There are many such criteria, and among them:

- Kind of activity;

- organizational and legal form - or LLC;

- amount of workers;

- the amount of income received;

- regional features of tax regimes;

- the cost of fixed assets on the enterprise's balance sheet;

- circle of main clients and consumers;

- export-import activities;

- preferential tax rate for certain categories of taxpayers;

- regularity and uniformity of income generation;

- the ability to properly document expenses;

- the procedure for paying insurance premiums for individual entrepreneurs in 2020 for themselves and for employees for LLCs and individual entrepreneurs.

If you want to avoid annoying financial losses, under any taxation system you must first of all properly organize your accounting. So that you can try outsourcing accounting without any material risks and decide whether it suits you, we, together with the 1C company, are ready to provide our users with a month of free accounting services :

Free accounting services from 1C

Absolutely all taxpayers can work on the general taxation system; OSNO is not subject to any restrictions. Unfortunately, this system is the most burdensome in Russia, both financially and administratively (that is, complex in accounting, reporting and interaction with tax authorities).

But for small businesses there are much simpler and more profitable tax regimes, such as the simplified tax system, UTII, Patent Taxation System, Unified Agricultural Tax. Such regimes are called preferential or special, and they allow a start-up or small business to operate in fairly benign conditions. You can familiarize yourself with these taxation systems in detail in separate articles dedicated to them.

To operate under preferential treatment, LLCs or must meet a number of requirements, such as:

| Requirements | simplified tax system | Unified agricultural tax | UTII | PSN |

| Kind of activity | The production of excisable goods (alcohol and tobacco products, cars, gasoline, diesel fuel, etc.) is prohibited; extraction and sale of minerals, except for common ones, such as sand, clay, peat, crushed stone, building stone. Prohibition of use by banks, pawnshops, investment funds, insurers, non-state pension funds, professional participants in the securities market, private notaries and lawyers. For a complete list, see Art. 346.12 (3) Tax Code of the Russian Federation. | Intended only for agricultural producers, i.e. those who produce, process and sell agricultural products. This also includes fisheries organizations and entrepreneurs. The main condition for applying the Unified Agricultural Tax is that the share of income from the sale of agricultural products or catch must exceed 70% of total income from goods and services. LLCs or individual entrepreneurs that do not produce agricultural products, but only process them, are not entitled to apply the Unified Agricultural Tax. Manufacturers of excisable goods (alcohol, tobacco, etc.) also cannot apply the Unified Agricultural Tax. | The following services are allowed: household, veterinary, catering, parking lots, trucking, service stations, etc., as well as some types of retail trade in areas up to 150 square meters. m. (a complete list of activities on UTII is given in clause 2 346.26 of the Tax Code of the Russian Federation). The specified list of activities may be reduced by regional laws. | Certain types of business activities specified in Art. 346.43 of the Tax Code of the Russian Federation, including services and retail trade (as well as catering services) on areas up to 50 square meters. m. This list can be expanded in the regions with additional types of household services for OKUN. |

| Organizational and legal form | LLCs and individual entrepreneurs, except for foreign organizations, government and budgetary institutions and organizations in which the share of participation of other organizations is more than 25% | Only LLCs and individual entrepreneurs of agricultural producers or fisheries. | LLCs and individual entrepreneurs, except for organizations in which the share of participation of other organizations is more than 25%, as well as categories of largest taxpayers | Individual entrepreneur only |

| Number of employees | No more than 100 | There are no restrictions for agricultural producers, and for fishing farms - no more than 300 employees. | No more than 100 | No more than 15 (including the individual entrepreneur himself and employees in other modes) |

| Amount of income received | An already operating LLC cannot switch to the simplified tax system if, based on the results of 9 months of the year in which it submits a notice of transition, its income exceeded 112.5 million rubles. There is no such restriction for individual entrepreneurs. Additionally, LLCs and individual entrepreneurs who received income in excess of 150 million rubles during the year lose the right to the simplified tax system. | Not limited, provided that the share of income from the sale of agricultural products or catch exceeds 70% of total income from goods and services. | Is not limited | An entrepreneur loses the right to a patent if, since the beginning of the year, his income from the type of activity for which the patent was received has exceeded 60 million rubles. |

Here we have provided only the most basic requirements for the application of preferential treatment; for complete information, please refer to the relevant articles on the website.

Algorithm for choosing a tax system

So, we have understood the main elements of Russian tax systems. What to do with all this? You need to assess which tax regimes your business meets.

- You need to start with the chosen type of activity, namely, the requirements of which taxation systems it fits into. For example, retail trade and services are subject to the simplified tax system, OSNO, UTII and PSN. Agricultural producers can work on OSNO, simplified tax system and unified agricultural tax. Organizations and individual entrepreneurs engaged in production cannot choose UTII and PSN. Individual entrepreneurs can purchase a patent for production services, such as the production of carpets and carpet products, sausages, felted shoes, pottery, cooper's ware, handicrafts, agricultural implements, eyewear, business cards, etc. The widest selection of special activities tax regimes - from the simplified tax system.

- There are few restrictions on the organizational and legal form (IP or LLC) - only individual entrepreneurs can acquire a patent, but the benefits of a patent for organizations can easily be replaced by the UTII regime if it is applied in the selected region. Other tax regimes are available to both individuals and legal entities.

- In terms of the number of employees, the patent tax system has the most stringent requirements - no more than 15 people. Restrictions on employees for the simplified tax system and UTII (no more than 100 people) can be called quite acceptable for starting a business.

- The estimated income limit for the simplified tax system is 150 million rubles per year; perhaps, it will be difficult for trade and intermediary firms to meet it. There is no such income limit for UTII, but only retail trade is allowed, not wholesale. Finally, the limit of 60 million rubles for the patent tax system is quite difficult to overcome given the limited number of employees, so this requirement can be called not very significant.

- If you need to be a VAT payer (for example, your main clients are VAT payers), then it is better to choose OSNO. But here you need to have a good idea of what the amount of VAT payments will be, and whether you can easily return the input VAT from the budget. In the situation with this tax, it is almost impossible to do without qualified specialists.

- The simplified tax system Income minus expenses option may, in some cases, turn out to be the most profitable in terms of the amount of single tax payable, but there is a serious bureaucratic point here - confirmation of expenses. In this case, you need to know whether you can provide supporting documents (for more details, see the article on the simplified tax system Income minus expenses).

- After you have selected several taxation options for yourself (we remind you that OSNO can always be on this list), it is worth making a preliminary calculation of the tax burden. It is best to turn to professional consultants for this, but we will give the simplest examples of calculations here.

Note: the examples below are conditional for ease of comparison (for example, UTII is calculated quarterly, and we compare annual tax amounts), but are suitable for comparing the tax burden.

In what cases is it beneficial to use OSNO?

Despite the fact that many enterprises are forced to use OSNO because they do not have the right to special regimes, there are those who deliberately do so.

First of all, OSNO is beneficial for companies and entrepreneurs who are involved in the VAT chain.

If a company works for OSNO and pays VAT, it is more profitable for it to buy goods and services from the same VAT payer, because he will issue an invoice with allocated VAT. The company will be able to deduct this amount and reduce its VAT payable. This is why large companies prefer OSNO counterparties and refuse to cooperate with those who apply a different regime. In order not to miss the “big fish,” it is sometimes more profitable to switch to a general taxation regime and endure the complexity of accounting.

In addition, it is beneficial for an organization to use OSNO if its type of activity falls under income tax benefits.

An example of comparing the tax burden under different regimes for an LLC

Solnyshko LLC plans to open a non-food store in the city of Vologda. The following data is available:

- estimated turnover, i.e. sales income per month – 1 million rubles (excluding VAT);

- estimated expenses (purchase of goods, rent, salaries, insurance premiums, etc.) per month – 750 thousand rubles;

- sales floor area – 50 sq. m;

- number of employees – 5 people;

- the amount of insurance premiums for employees per month is 15 thousand rubles.

By type of activity, a non-food store (taking into account the fact that it is an LLC, a patent would also be possible for an individual entrepreneur) satisfies the requirements of the following taxation systems: UTII, simplified tax system and OSNO. Since Solnyshko LLC complies with the restrictions established for preferential regimes, we will compare only UTII, STS Income, STS Income minus expenses. OSNO is not included in the calculations, as it is clearly an unprofitable option.

1. For UTII, income and expenses are not taken into account, and the imputed tax is calculated using the formula: BD * FP * K1 * K2 * 15%:

- DB for retail trade is equal to 1800 rubles,

- FP – 50 (sq. m),

- K1 for 2020 - 1.915,

- K2 for the city of Vologda is equal in this case to 0.52.

The amount of imputed income will be 89,622 rubles per month. Let's calculate UTII at a rate of 15% - equal to 13,443 rubles per month. In total, UTII for the year will be 161,320 rubles. This amount can be reduced by paid insurance premiums and employee benefits (15 thousand rubles * 12 months), but not more than half. The annual amount of UTII payable will be 80,660 rubles (we remind you that UTII is calculated and paid quarterly).

2. For the simplified tax system Income, the calculation of the single tax looks like this: 1 million rubles * 12 months. * 6% = 720,000 rubles. This amount can also be reduced by paid insurance premiums and employee benefits (15 thousand rubles * 12 months), but not more than half. We calculate: 720,000 – 180,000 (insurance contributions for employees per year) = 540,000 rubles of single tax payable for the year.

3. For the simplified tax system Income minus expenses - the usual tax rate in the Vologda region is 15%. We calculate: 12 million rubles (income for the year) minus 9 million rubles (expenses for the year) = 3 million rubles * 15% = 450,000 rubles of single tax payable for the year. We cannot reduce this amount at the expense of insurance premiums; we can only take the contributions into account in expenses.

Note: the calculation and payment of the single tax on the simplified tax system occurs in a slightly different order - through the payment of advance payments quarterly, but this does not affect the annual total tax amount.

Total: The most profitable option in this particular case turned out to be UTII .

Does this mean that UTII is the most profitable regime for all trading enterprises? Of course not. Let's change the calculations a little. Let, for example, K2 in the formula be 0.9 (we remind you that K2 is established by regional laws), then the annual amount of imputed tax payable will already be 139,603 rubles . And if the store’s revenue is not 1 million rubles, but 300 thousand rubles per month, then the single tax on the simplified tax system for income will be 108,000 rubles, while the amount of UTII does not decrease with a decrease in turnover, because calculated on the basis of a physical indicator, in this case sq. m.

If we also assume that even such a rather modest turnover will not reach the store in the first month of its operation, then the UTII payer must still pay a fixed estimated amount of tax from the first day of registration, while the simplifier will begin to calculate the single tax only with the beginning of income generation. Taking into account this situation, the simplified tax system for income becomes more profitable. That is why a novice businessman, when the real income is still unknown, is recommended to work on the simplified tax system.

We draw the attention of all LLC-organizations can pay taxes only by non-cash transfer. This is a requirement of Art. 45 of the Tax Code of the Russian Federation, according to which the organization’s obligation to pay tax is considered fulfilled only after presentation of a payment order to the bank. The Ministry of Finance prohibits paying LLC taxes in cash. We recommend that you open a current account on favorable terms.

Combination of modes

What if you want to conduct several lines of business, for example, retail sales in a store and the provision of trucking services? You can combine tax regimes. Let's assume that the store, with a small area, gives a good turnover. To reduce the tax burden, it can be transferred to UTII or PSN (for individual entrepreneurs), and transportation that is carried out from time to time can be subject to a single tax on the simplified tax system. If, on the contrary, transportation brings a stable income, and trade in a store has ups and downs, then it is more profitable to conduct transport services on UTII, and trade on the simplified tax system.

What modes can be combined? Various combinations are possible: OSNO and UTII, simplified tax system and UTII, PSN and simplified tax system, PSN and UTII, etc. But there are also prohibitions: they do not combine OSNO and UTII, OSNO and simplified tax system, simplified tax system and UTIC.

And when choosing a taxation system, it is imperative to take into account regional characteristics. Potentially possible annual income for PSN, K2 for UTII, the size of the differentiated tax rate for the simplified tax system. Income minus expenses is set by local authorities. Sometimes in neighboring cities that are similar in purchasing power, but located on the territory of different municipalities, the amount of taxes payable under preferential regimes may differ several times. Maybe in your case it is worth considering the possibility of opening a business in a neighboring area?

Thus, the choice of tax regime depends on many nuances. In your specific case, we recommend contacting specialists who will offer a tax option specifically for you, taking into account the prospects of your business. We give only general recommendations on choosing a tax system.

Who is the traditional tax format suitable for?

Today, absolutely any company and individual entrepreneur can work under the general tax exemption regime. In order to be guided by the ORN, you do not need to take absolutely any actions (in particular, collect a bunch of documents). As noted earlier, the transition to ORN occurs automatically. All you need is state registration of the company.

This regime has the following features that you need to remember when choosing a taxation format:

- minimum number of tax benefits;

- complex accounting scholarship that requires a professional accountant on staff;

- the presence of a large number of tax exemptions.

Therefore, only those enterprises whose business is firmly on its feet and can withstand such strong tax pressure can use ORN. This requires high self-sufficiency of the organization. Changing the regime to a special one is possible only if the organization meets all the conditions for the transition. And such a transition is possible only once a year.