The essence of capitalization

A deposit with interest capitalization is the same as a bank deposit, but its peculiarity is that periodically accumulated interest is added to the total amount of the deposit. After this, interest is charged on the entire amount. Capitalization of interest on the account ensures maximum income from investments.

Most often, interest is capitalized monthly, but it happens that the bank offers ready-made programs with other frequencies. Only once every quarter or six months. Monthly capitalization is more profitable for the client.

Pros and cons of capitalized deposits

To contents

Capitalization of interest on a deposit account has its advantages and disadvantages. It is clear that the main advantage is the additional profit due to interest on what has already accrued. Also, interest rates are usually high, since a significant amount is being invested for a long time. But there are banks that deliberately set the interest rate on a capitalized deposit a little less than on regular deposits. For this reason, it is impossible to say for sure that a capitalized investment is always more profitable than a standard deposit.

Fact! The main disadvantage of capitalized investments is the imposition of restrictions on the mobility of funds.

That is, it is impossible to use your own money throughout the entire period of the agreement. If you decide to close your account, you will not receive the money you originally expected. Some financial institutions prescribe such conditions that the client loses a decent share of income or even all of it. The most loyal ones, in case of early closure of the account, accrue interest according to the traditional scheme without capitalization.

You need to understand that the frequency of interest accrual and their capitalization are two different things. So, accrual can occur every month, but addition to the deposit amount can be done quarterly. This point should definitely be checked in the terms of the bank offer.

Types of capitalization

Different deposits with interest capitalization differ only in the timing of adding interest to the total amount of the deposit in the account:

| Type of deposit | Description |

| One-time | The bank makes a one-time capitalization only at the end of the term in the case when the client extends the validity of the deposit. Financial organizations came up with this trick specifically to make investors keep their funds on deposit longer. Because in this case, the depositors' money gives the institution more sources to lend to other clients. |

| Daily | This type of capitalization is rarely chosen. When the interest on the deposit and the amount are too small, then the income will increase almost imperceptibly. But with large amounts and high interest, such interest calculation will be the most profitable. |

| Monthly | This is the most common type of deposit with capitalization. Interest is accrued monthly; most often, this capitalization is chosen for deposits for up to six months or a year. |

| Quarterly | A deposit with interest accrued every 3 months is selected for a deposit with a validity period of 3 to 12 months. It is imperative that the total number of months for which the deposit is made is a multiple of 3. |

| Semi-annual | Rare type of interest accrual. Capitalization occurs once every 6 months. If the contract is terminated before the end of six months, most of the accrued interest is lost. To get the maximum benefit, you will need to place money for a long period. |

| Annual | For small deposit amounts this type of capitalization is useless. It is chosen only for large and long-term investments for a period of 2 to 5 years. In this case, it is important to pay attention to the rate and recalculate the final benefit. In some cases, it turns out that monthly accrual is more profitable than annual accrual. |

The most popular options are deposits with monthly and quarterly capitalization.

Why do you need a contribution?

Russians love deposits for their reliability - and the guarantees that investing in bank deposits provides. For a very large part of the population, bank deposits, unfortunately, are the main investment tool:

However, there is one big “BUT”...

Can investing in a bank deposit be called investing? The main idea of investing is to maintain or increase the purchasing power of the funds that we invest in various financial instruments.

Does a bank deposit cope with this task? In most cases, unfortunately, no. Because interest rates on deposits are often lower than inflation. This means that the purchasing power of the funds deposited decreases over time. And our capital is melting.

But since a bank deposit cannot be called an investment instrument, in what situations should it be used? Below are a number of situations in which using a bank deposit would be reasonable.

Securing your liquidity

One of the mandatory elements of family financial security is the necessary liquid reserve. This is free money that a person or family can use at any time.

Often this cash reserve is also called a financial airbag. Because cash smooths out sudden blows of fate and helps the family overcome difficult times.

I talked about what this reserve should be and where it is best to store it in my video, turn on:

So, part of your reserve should be placed in a bank account. Most often, this is a bank account with a bank card linked to it, so that funds can be withdrawn from the account if necessary at any ATM. A convenient means of storing your own liquid fund is the first reason why you might need a bank deposit.

Of course, your financial safety net can also be stored on a deposit with interest capitalization. However, if you withdraw some of the money from the account before the end of the deposit, then in most cases the bank will charge you interest at the demand rate.

However, we should not be discouraged by this. Because we create a liquid reserve so that it ensures our financial security. We do not set ourselves the task of obtaining a high interest rate on these funds. If you can do this, great! And if it doesn’t work out, it doesn’t matter; After all, with the help of these means we ensure our own financial stability, and do not strive to earn money.

So, the first reason to have money in a bank account is to ensure your own liquidity. So that we can react flexibly to unforeseen situations, of which there are many in life.

By the way, a financial cushion is only one of three mandatory elements that provide our family with financial security. I talked about two other very important elements of financial stability in my short video - turn on:

Deposit as a means of short-term savings

A bank deposit is well suited for short-term savings. For example, a family would like to save 1,000,000 rubles for a new car. And for this purpose she is ready to save 50,000 rubles monthly.

It will take 20 months, or just under two years, to achieve the goal. For such purposes, a deposit with the possibility of replenishment is suitable. If it also includes capitalization of interest on the deposit, that’s great, because in this case the family will reach its goal a little faster.

However, the question arises: where is the line that separates short-term savings from medium- and long-term savings? From the point of view of personal financial planning, I would classify savings from 3 to 10 years as medium-term savings, and over 10 years as long-term savings.

If your savings horizon is less than 3 years, most likely only a bank deposit is suitable for this purpose. Because alternative investment options for such short periods will be associated with high risk.

So, a tool for short-term savings is the second reason why you might need a bank deposit.

An extremely conservative savings tool for mature adults

Finally, the third option is to use a bank deposit as a very conservative savings tool. This is often resorted to by very mature people, pensioners - who have already finished their careers.

They deposit their savings in a bank account to earn interest. In many cases, the capitalization of a bank deposit is no longer of interest to them - because they spend the interest they receive. And thus they organize an annuity for themselves, an addition to a small state pension.

They find what they need in the bank. This is the security of deposits, which are guaranteed by the state within certain limits. And also the predictability of receiving interest on the deposit, which forms an additional source of income for these people.

Download the PDF review “Personal Financial Planning” to invest wisely and create personal capital:

Three reasons to use a bank deposit

So, the main reasons for using bank deposits are:

- Storing all or part of your financial safety net in the bank;

- Using a deposit with the possibility of replenishment for short-term family savings;

- A very conservative savings instrument for mature people who have completed their careers.

Please note that above we are talking about the reasons for using deposits. These are accounts on which the bank charges interest. And this interest income is the main motive for opening such accounts.

Of course, along with deposit accounts, each person has several card and current accounts (also called demand accounts). We need them for non-cash payments, as well as receiving funds to your personal account. However, this article only discusses deposit accounts and the interest income they can generate.

But now interest rates on deposits are very low. And so a reasonable question arises: are there any alternatives to bank deposits?

If we talk about the first task, ensuring your own liquidity, then there is no replacement for a bank account/deposit to solve this problem. If you may need money urgently, it should either be in the form of cash or in a bank account.

Also, for short-term family savings, it is unlikely that anything can successfully replace a bank account. This is the most convenient tool for such tasks.

But for conservative investors to receive interest income on their savings, there is a very good replacement.

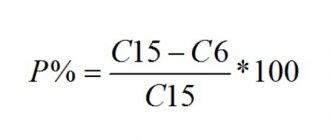

Formula for calculating interest capitalization

The general formula for calculating the capitalization of interest on a deposit account is as follows:

Dv = C * (1 + Rp)* T.

Дв - the total income from the capitalization of interest on the deposit together with the original amount that the depositor deposited into the account. C is the amount that the client invested in the financial institution. Рп - the amount of the interest rate per year, which is indicated in the agreement when opening a deposit account. T is the validity period of the bank deposit.

Using this formula, it is convenient to calculate only income from deposits with annual capitalization of interest.

To calculate income with monthly capitalization, use the formula Дв = С * (1 + Рп/12)Т , where Т is the number of months.

To calculate profit with daily capitalization: Дв = С * (1 + Рп/365)Т , where Т is the number of days the deposit is valid.

With quarterly capitalization: Дв = С * (1 + Рп/4)Т , where Т is the number of quarters for the deposit.

Profitability

The interest rate and overall return on the deposit are influenced by several factors:

- deposit amount (after 100,000 rubles in Sberbank it increases, and then after 400,000 and 700,000 rubles);

- currency in which the deposit is opened;

- deposit term (longer period means higher interest rate);

- the method in which the deposit was opened (if you do this yourself through Internet banking, profitability will increase).

You can calculate your profitability in advance if you take into account all the factors on which it depends.

Why is the income from the deposit decreasing?

The main goal of banks' financial activities is to make a profit, so they often develop schemes for inattentive depositors. Managers are silent about some pitfalls that prevent them from getting the maximum profit from a bank deposit. Basically, income decreases due to fees for services that are not discussed right away, but they are spelled out in the contract. These may be payments for:

- depositing money into an account;

- deposit account maintenance;

- return of deposit in cash;

- Internet banking, mobile application or SMS service;

- withdrawal of funds from the deposit and interest on the deposit;

- conducting bank deposit transactions;

- withdrawing money from an ATM.

Read the contract carefully before signing it. This will help you avoid additional expenses or imposed services. Careful study of documents before opening a deposit with capitalization will significantly reduce risks and losses.

Features of capitalization in Sberbank

Sberbank of Russia has developed many deposit options with different conditions for its clients. Even with a minimum amount of free money (1000 rubles), a person can open a deposit and receive passive income. But in order to earn money, you need to understand the nuances of the contract.

The client must understand that the main condition for capitalizing a deposit with Sberbank is a ban on withdrawing funds before the end of the period specified in the agreement. They remain untouchable in any case. Having deposited a deposit in a bank, a person must forget about these funds for a certain time.

Advantages and disadvantages

Among the advantages of deposits with capitalization are:

- obtaining maximum income by adding interest to the total amount of the deposit and further accruing interest on the new increased amount;

- When opening a deposit for a long time and with a large amount of money, the financial institution offers increased interest.

Upon termination of the agreement to open a bank deposit with capitalization, the investor receives income only from interest accrual, without capitalization. But the main disadvantage of such deposits is that it is impossible to carry out transactions with money on deposits with capitalization.

How to choose a deposit

- When choosing a deposit program, you must initially determine the investment goals and the need for them. If the investor needs to constantly manage the funds accrued in the deposit account, then the deposit with interest capitalization will not bring much income, since profit will be generated only from the main part of the invested funds. If an individual has enough free funds that he is ready to place for a long term, then deposits with interest capitalization are the optimal program for obtaining additional income.

- Interest Rates: The higher the deposit amount and the longer the term, the higher the interest rate provided to the depositor. Maximum rates are usually offered for deposits with interest accruing at maturity. In this case, the maximum income will be received when the contract is extended.

- Security: when choosing a credit institution, you need to familiarize yourself with the bank’s reputation, as well as the availability of funds insurance. For example, Sberbank PJSC is included in the register of banks at the Deposit Insurance Agency. The maximum amount of compensation for each separately opened deposit is 1.4 million rubles.

Capitalization of interest or payments upon maturity

The choice of deposit type depends on your needs and interest rate. For deposits with capitalization, interest is calculated periodically and added to the amount. So the following interest will be added to the increased deposit amount. This way, the final income is greater than with a deposit without capitalization.

If you know in advance that income from an investment will need to be withdrawn monthly, there is no point in opening a deposit with interest capitalization. In this case, it is better to make a regular deposit. But if it is more important to get the maximum amount of income, then opt for capitalization of the interest rate.

Some credit institutions offer clients a deposit with capitalization and the opportunity to withdraw funds before capitalization. In practice, it often turns out that lower rates apply to deposits with interest capitalization. In this case, there may be no benefit at all or it will be very insignificant. Calculate your own benefits for different types of deposits to find the most profitable option.

Rates on deposits with simple interest and with interest capitalization

Financial analysts argue that rates on deposits with simple interest, that is, those that do not involve their capitalization, are usually higher than on “capital” deposits. On average, their difference can reach up to 2% in the same bank and, naturally, not in favor of the latter.

Experts note that at the moment, capitalization of interest allows you to increase the profit of the deposit by an average of 0.3 to 0.4% per annum.

But if the benefits are not great, why offer such a banking product at all?

It turns out that a regular deposit with a classic interest payment scheme (on the day the contract expires) is conservative. Its main advantage is a high rate, and its disadvantage is the lack of flexibility in managing funds placed on the account:

- firstly, there is no possibility of early termination of the contract without loss of interest, and therefore profit;

- secondly, it often cannot be replenished.

From this we can conclude that deposits with a regular payment scheme are suitable for depositors who can easily do without invested funds until the end of the contract with the bank. That is, set it and forget it.

Now let's move on to “capital” contributions. Their main advantage is that they are easier to manage. This product is more democratic and is suitable for those who want to maintain access to their money and, at the same time, receive, albeit not high, income.

Remember the pattern: if a bank has enough money, but they issue few loans, then they have no special interest in deposits, which is reflected by lowering the rate. If there is little money, then banks raise rates to attract financial flows.

Top 3 banks with deposit capitalization

To understand which bank to open a deposit with, you will need to compare their products. Conditions for the Gazprombank deposit “Your success”, “For life” and “Pension savings”:

| Contribution | Bid | Minimum term | Deposit and withdrawal | Interest payment |

| Your success | 7,05% | 367 days | No | In the end of the month |

| For life | 5,30% | 91 days | No | In the end of the month |

| Pension savings | 5,90% | 91 days | No | At the end of the year or upon expiration of the deposit term |

Conditions for MKB deposits “All inclusive investment”, “All inclusive maximum income” and “All inclusive settlement”:

| Deposits | Percent | Minimum term | Partial withdrawal | Interest payment |

| Investment | From 5.6% | 3 months | No | Monthly |

| Maximum income | From 5.9% | 3 months | No | Monthly |

| Calculated | From 5% | 3 months | To the minimum balance | Monthly |

Conditions for Sberbank deposits “Manage”, “Replenish” and “Save”:

| Contribution | Minimum percentage | Minimum term | Minimum deposit amount | Partial withdrawal | Partial replenishment |

| Manage | 3,15% | 3 months | 30 thousand rubles | Yes | Yes |

| Replenish | 3,45% | 3 months | 1 thousand rubles | No | Yes |

| Save | 2,95% | 1 month | 1 thousand rubles | No | No |

Interest rates on deposits are insignificant, so many Russians are looking for alternative ways to earn money on their savings. This could be an individual investment account or a brokerage account. Read about how to invest money without losses on our portal.

The main differences between annuity contracts and deposits

What are the main differences between such contracts for receiving rent from bank deposits? I would draw your attention to the following aspects.

- Higher interest rates

In Fixed Income contracts and similar ones, interest rates are significantly higher than current deposit rates. And therefore, if your goal is to receive high interest on invested funds, then an annuity contract may be a very suitable solution for you.

- Fixed interest rate for the entire term of the agreement

In banks, it is very rare to find multi-year deposits in which the interest rate on the deposit would be fixed for several years at once. Most often, banks offer deposits up to a year, reserving the right to change the deposit rate when prolonging the deposit.

However, in specialized contracts for the formation of annuity, the interest rate is fixed for the entire term of the contract, and then does not change. This gives us the opportunity to reliably and profitably place capital for a period of 3-5 years with regular interest accrual on invested funds.

- Limiting the liquidity of your funds

You need to understand that annuity contracts are not bank accounts. If necessary, you will not be able to urgently close the contract and immediately receive all the money invested.

Because in these plans there are certain penalties for early cancellation of the contract. And therefore you cannot invest all your funds to accrue interest. You must have a sufficient liquid reserve in case of various force majeure circumstances.

- Large amounts of replenishment

If your contribution includes the possibility of replenishment, then often there are no restrictions on the size of the additional contribution, or these restrictions are very small. In Fixed Income, the minimum additional contribution amount is 10,000 USD or higher.

- Certain costs

Most often, bank deposits do not involve any costs - you simply place funds in the account and periodically receive interest on the deposit. Contracts for receiving provide certain commissions.

And therefore, the use of such plans is justified for fairly large amounts. So that the difference in interest rates covers the fees for conducting such a contract.

Analogue of a deposit with capitalization

For those who do not want to open a deposit, but want to receive a small income on the account balance, banking institutions offer special debit cards. Banks charge interest on the minimum balance. At the same time, you can freely make any transactions, spend money and replenish your balance. The main thing is that a certain amount remains on the card at all times. The income is approximately 3-4% per year.

In particular, Sberbank provides such a service with a debit pension card. The financial institution charges 3.5% per annum on the balance of funds.

about the author

Klavdiya Treskova - higher education with qualification “Economist”, with specializations “Economics and Management” and “Computer Technologies” at PSU. She worked in a bank in positions from operator to acting. Head of the Department for servicing private and corporate clients. Every year she successfully passed certifications, education and training in banking services. Total work experience in the bank is more than 15 years. [email protected]

Is this article useful? Not really

Help us find out how much this article helped you. If something is missing or the information is not accurate, please report it below in the comments or write to us by email

Comments: 0

Your comment (question) If you have questions about this article, you can tell us. Our team consists of only experienced experts and specialists with specialized education. We will try to help you in this topic:

Author of the article: Klavdiya Treskova

Consultant, author Popovich Anna

Financial author Olga Pikhotskaya