For whom is registration of a cash book mandatory?

The main legal act regulating the maintenance of cash books by Russian organizations is Bank of Russia Directive No. 3210-U dated March 11, 2014 (hereinafter referred to as the Directive).

NOTE! As of August 19, 2017, changes have been made to the cash register procedure. Read more about them:

- “Changes in the procedure for conducting cash transactions”;

- "New rules for working with accountables."

The main part of its provisions (including those directly related to the maintenance of cash books) came into force on 06/01/2014. In accordance with them, registration of cash books is mandatory for all enterprises carrying out certain transactions with cash, regardless of the form of taxation applied.

The use of online cash registers does not relieve the obligation to maintain a cash book.

What it is and why online cash registers were introduced, read here.

Yes, with the transition to online cash registers, the need to maintain some primary cash register has disappeared. It is now being replaced by fiscal documents that are generated and stored electronically. But this does not apply to the cash book. It is conducted through the so-called “main cash register”, in which not only settlements with customers take place, but also other cash turnover. Therefore, you need to maintain a cash book as before.

Read more about this in the article “Do I need a cash book to maintain an online cash register?”

The cash book may not be legally filled out by individual entrepreneurs who, in accordance with the established procedure, keep records of income, expenses, physical indicators and other taxable items that characterize a particular type of commercial activity (clause 4.1. Instructions). Since individual entrepreneurs are almost always required to keep records of income and expenses (both under OSN, and under Unified Agricultural Tax, Simplified Tax System, PSN) or physical indicators (with UTII), this norm can be legitimately interpreted as applying to all individual entrepreneurs.

For more information about keeping records of income and expenses by individual entrepreneurs, read the article “How to keep a book of income and expenses under the simplified tax system (sample)?” .

ConsultantPlus experts explained the rules for working with the cash book in various situations:

If you don't have access to the system, get a free trial online.

Our task in this article is to explore how to fill out a cash book, consider a sample algorithm for entering data into it, and the procedure for handling the corresponding document.

Rules

Let us consider in more detail the provided rules for filing the cash book.

If the document implies a standard journal, which is printed according to the established form KO-4 (approved by Decree of the State Statistics Committee No. 88 of August 1998), where all sheets without exception are horizontal, it will be necessary to stitch according to the instructions indicated below.

The main feature of maintaining such documentation is that each page inside the journal includes several parts, one of which remains in the book, and the second must be torn off and attached to other reports directly by the cashier himself.

The information on both sides of the page must be identical, and this can be done using carbon paper. Based on this, the numbering of sheets is subject to duplication.

In such a situation, that part of the sheets that is in the binding is subject to stitching (part of the sheet can be stapled or simply glued). In the process of filling out such a cash book, a manual option is often used to indicate all the necessary information. The pages must be numbered, and the document itself must be stitched and bound at the beginning of its maintenance.

In a situation where the cash book is generated by machine, in other words, all the necessary information is indicated instantly by the responsible person into an accounting program, for example in 1C: Enterprise or another (the book can be maintained in a standard program like MS Excel), it is necessary act differently.

At the end of the working day, when cash transactions occurred, information entered into the document based on incoming and outgoing orders, the responsible person is obliged to print the page generated in the software.

The page or pages must be printed in several copies: 1 – loose leaf of the document, 2 – report of the responsible employee.

Loose sheets and reports of the responsible sheet must be numbered. Moreover, the numbering should begin from the beginning of the calendar year (month, quarter, etc.).

In addition, loose sheets and duplicate reports of the responsible sheet, generated on separate unstitched sheets, according to the legislation of the Russian Federation, can be maintained not only by software, but also generated by hand. However, in the second option it is necessary to place carbon paper.

According to established rules, the document is maintained from the beginning of the calendar year. All options established in the organization for maintaining and forming a cash book must be reflected in the accounting policies and be recorded separately by a management order.

At the end of the calendar month/quarter, the authorized employee is obliged to display on the last sheet for a certain period how many pages were generated from the cash book in this calendar month/quarter. Without exception, all loose sheets that were signed by a verified responsible person must be kept in his custody until the end of the year.

As they accumulate, the sheets are subject to stitching and further stitching.

On the back of the last page, the thread used to stitch the sheets must be sealed with a seal indicating the total number of stitched pages. A seal impression must be affixed, which affects the seal and at the same time remains on the last page of the book.

The generated cash book in the software does not require printouts and stapling according to the legislation of the Russian Federation. Registration is carried out using technical means that fully protect against unauthorized access. All you need is confirmation with a digital electronic signature.

The above rules must be remembered to minimize the risk of making a mistake and, as a result, receiving penalties.

Additionally, it is worth paying attention to the fact that, unlike the cashier-operator’s journal, the document in question does not need to be registered with the territorial representative office of the tax service.

How to maintain a cash book?

The cash book must be maintained by the organization in the KO-4 form, approved by Decree of the State Statistics Committee No. 88 of August 18, 1998 and corresponding to number 0310004 in OKUD (clause 2 of the Directive). You can download it on our website:

You only need to fill out the cash book on those days when the organization actually received (issued) funds.

For information about the procedure that should be followed when conducting cash transactions, read the material “Procedure for conducting cash transactions in 2020.”

NOTE! From August 19, 2017, the cashier does not have to make entries in the cash book. This can be any authorized employee of the organization, for example, an accountant. The corresponding change to the cash procedure was made by the Bank of Russia’s instruction dated June 19, 2017 No. 4416-U ( what else has changed, see here ). But later in the article we will continue to habitually call such an employee a cashier.

There are 3 ways to fill out cash books:

- manually on prepared forms;

- on a computer (with subsequent printing);

- on a computer with saving the cash book file in the software registers.

Next, we will look at the nuances of using each method in more detail. For now, let’s study the structure of the cash book and how the fields are filled in.

A completed sample cash book can be downloaded from our website.

Help report from cashier-operator and online cash register

The primary unified forms for recording trade operations, including Form No. 6-KM, were approved by State Statistics Committee Resolution No. 132. The cashier's certificate report contains readings from check-total counters, the amount of revenue received per day or shift, and the amount of cash refunds to customers. Since the unified forms of Goskomstat are no longer mandatory for use, the cashier-operator’s report can be filled out on a form of his own design in compliance with the mandatory details. The cashier's report and a sample of how to fill it out can be found at the end of this article.

Companies and individual entrepreneurs using online cash registers may not fill out the unified forms KM-1 - KM-9, approved by Resolution No. 132, which includes the “Cashier’s Certificate Report” in form KM-6. The Ministry of Finance of the Russian Federation gave such an explanation in its letters dated 09/16/2016 No. 03-01-15/54413, dated 06/16/2017 No. 03-01-15/37692 and dated 07/04/2017 No. 03-01-15/42314. The department explains this approach as follows: Resolution of the State Statistics Committee No. 132 does not apply to the legislation on the application of cash register systems, consisting of Law No. 54-FZ dated May 22, 2003 and regulations adopted in accordance with this law; therefore, the resolution does not apply to online cash registers Necessarily.

The need to fill out a cashier-operator report with the introduction of an online cash register also disappears due to technical reasons: all the required information and indicators are stored in the cash register’s fiscal storage device, from which it is not difficult to generate reports. Tax officials even receive information about cash transactions made through online cash register systems in real time.

Cash book structure (rules for filling out fields)

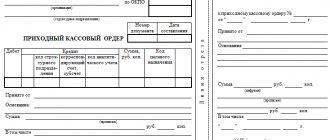

The cash book corresponding to form No. KO-4 contains 3 types of pages:

- front (sample cover or title);

- internal (pages 3 to 10);

- final (located at the end of the document).

The front pages contain information about the company, as well as the year for which the cash book reflects cash transactions. The internal pages of the document contain the following columns:

- “Cash for” (it records the dates of certain transactions with funds);

- “Sheet” (the serial number of a specific sheet of the cash book is indicated here);

- “Document number” (this column records the order number - incoming or outgoing);

- “From whom received or issued to” (initials of the person or company that deposits or receives cash);

- “Number of the corresponding account, sub-account” (this column records the account that corresponds in the prescribed manner with account 50, individual entrepreneurs do not fill out this area of the cash book);

- “Receipt” (the amount of funds on receipt orders is recorded);

- “Expenses” (indicate the amount of funds for settlement orders);

- “Total for the day” (receipts are summed up, as well as cash payments for the cashier’s work shift);

- “Cash balance at the end of the day” (the amount of the cash balance is indicated).

In the “Transfer” column of the cash book, the total amount of funds for orders of both types can be recorded, reflected in a specific table, so that the cashier has the opportunity to continue entering information on the next page.

The following signatures must appear at the end of each internal page of the cash book:

- the cashier of the organization, who fills out basic information in the cash book;

- an accountant (who simultaneously indicates the number of PKOs and RKOs, and also certifies the fact that he received and checked the orders).

On the last (final) page of the document, it is indicated how many sheets are stitched and numbered, the date of compilation of the cash book, and also the signatures are affixed:

- chief accountant;

- head of the company.

Procedure for maintaining a cash book

The cash book is an important document for LLCs and individual entrepreneurs, who in their work deal with the receipt of cash. When conducting it, you must be guided by the following basic rules:

- The book is started and used in the activities of the enterprise for one calendar year .

- The book is maintained either by the chief accountant or by the person who replaces him (most often this is the cashier) .

- One organization can maintain only one cash book , regardless of how many types of activities and taxation systems it uses. An exception is the situation with subsidiaries - they maintain their own separate book, a copy of the sheets of which is transferred to the company's head office at the end of the year.

- The cash book displays all transactions of the enterprise - both incoming and outgoing. The basis for entering data is PKO and RKO (receipt and expense cash orders, respectively).

- If on a certain day no operations were performed at the enterprise, then the sheet of the ledger remains blank .

- There are two forms of maintaining a cash book - electronic and paper . The rules for filling it out directly depend on the chosen form.

- Data is entered into the book immediately after the actual receipt or expenditure of funds .

- The cash book has a legally approved form KO-4 .

- At the end of each day in which cash transactions were carried out, all data entered in the book is verified with the indicators of cash orders. Afterwards, the final cash balance is displayed, which is checked against the amount of cash in the cash register.

The total amount is signed by the cashier or other person responsible for maintaining the book.

Also, the calculated indicators for each day are checked by the chief accountant of the enterprise, which is confirmed by his signature at the end of the sheet. The listed rules relate rather to organizational issues related to maintaining a book. Next, it is worth considering in more detail the order of its registration.

Filling out the cash book manually (sample algorithm for working with a document)

The procedure for manually maintaining a cash book requires stitching and numbering it before entering data. The main feature of the paper version of the cash book is that the document is divided into 2 parts - the main and detachable ones.

When starting a shift, the cashier must place the tear-off part of the cash book under the main one, and place carbon paper between them. Then you need to record the cash balance as of the beginning of the day. During the shift, data on PKO and RKO should be recorded in the cash book - according to the columns that we discussed above.

At the end of the shift, the cashier must count all the turnover for PKO and RKO for the day and record them in the cash book, put his signature on the document, and then take it along with the orders to the accountant.

Read about sanctions for violating the rules for conducting cash transactions in the article “Cash discipline and responsibility for its violation.”

Cash book: sample manual filling and filling requirements

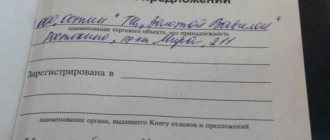

Maintaining a cash book in 2020 begins with numbering and stitching its sheets. The ends of the lacing at the back of the journal must be sealed with a paper strip on which you must indicate the number of sheets, the start date of maintaining the cash book and the end date. To certify the record, the chief accountant and the head of the organization must sign, and a seal, if available, must be affixed. It should look like this:

On the title page of the cash book you must indicate the name of the organization and the period for which the document was opened. All entries must be made only with blue or black ballpoint pen or ink.

Each sheet is divided into two parts:

- one remains in the book;

- the second is detachable and is stored together with the RKO and PKO registers.

To fill out the sheet, the cashier places carbon paper so that the entry in pen is on the sheet that remains in the document. The entries must be completely identical, but you cannot sign a carbon copy. Therefore, at the end of the day, the cashier must sign on each copy of the cash book. All records about cash settlements and cash settlements are entered line by line in the appropriate columns, indicating the details of the person who deposited or received the money. Income and expense are entered in different columns. If one sheet is not enough to reflect all transactions for one day, the cashier must fill out the “transfer” line, which records the total amount of money received and spent at that moment. The next sheet of the cash book begins with the same amounts.

At the end of the day, you should sum up the results and indicate the total turnover at the cash register for the day and withdraw the remaining cash at the end of the day. If the cash register included amounts intended for the payment of wages or benefits according to the payroll or payroll, the cashier must allocate them in the line “including wages, social payments and scholarships.” After all the entries have been made, they are checked against the primary documents and certified by the chief accountant.

A correctly completed cash book sheet for the day looks like this:

How to fill out the KO-4 cash book on a computer?

Filling out form No. KO-4 on a computer can be done using an accounting program or an office application (for example, Excel). After entering the necessary information into the cash book on the PC in accordance with the algorithm we discussed above, the cashier needs to:

- print all pages of the cash book;

- sign 2 copies of the document and take it to the accountant, taking with you the PKO and RKO, issued for the day.

Every year, all printed sheets of the cash book should be stitched and numbered (in the case of filling out the form manually, as we noted above, they must be stitched and numbered initially), and then a scheme for filling out the cash book should be sent to the chief accountant and manager for signature

Firms have the right to fill out and maintain a cash book without printing it out (clause 4.7 of the Instructions), generating the corresponding document entirely in electronic form. This feature can be used if the cash book compiler has at his disposal technical means that guarantee:

- protection against unauthorized access;

- no errors when entering data into the cash book;

- protection against information loss.

Electronic samples of cash books must be signed with an electronic signature that meets the requirements of Federal Law No. 63 of 04/06/2011. A virtual sample of a cash book may differ from form No. KO-4 in appearance, but the columns in it will be the same.

See also “Procedure for making corrections to the cash book (nuances)” .

Where to download the cover page of the cash book

The form of the title page of the cash book, as well as all other pages of the KO-4 form can be downloaded on our website.

Here you will also find a sample of filling out the title page of the cash book. You can also download it and, saving it on your computer, fill out your document according to our example.

Results

A cash book is a mandatory document when working with cash, be it revenue or other payments. Its form and procedure are strictly regulated, and violations when working with it may result in liability. Therefore, it is very important to maintain this cash register accurately and without errors.

Sources: Directive of the Bank of Russia dated March 11, 2014 N 3210-U

You can find more complete information on the topic in ConsultantPlus. Full and free access to the system for 2 days.

Features of the use of the unified form KO-4 in 2019

Since the beginning of 2013, the forms of primary documents contained in albums unified by Goskomstat have become optional for use. However, if we are talking about primary documents and registers, the forms of which are also established on the basis of other federal laws (in particular, this directly concerns documents on cash transactions), the developed unified form remains mandatory.

This is exactly what is stated in the information of the Ministry of Finance of Russia dated December 4, 2012 No. PS-10/2012 about the entry into force of the accounting law in 2013. Despite the fact that from June 1, 2014, a new procedure for recording cash transactions was established (directive of the Bank of Russia dated March 11, 2014 No. 3210-U), the form of the cash book remained unchanged. At the same time, individual entrepreneurs may not maintain this form of accounting register (clause 4.6 of the Bank of Russia Directive No. 3210-U dated March 11, 2014).

The correctness of maintaining the cash book is monitored by the chief accountant or accountant, and in their absence, the manager.

For information on how cash transactions are reflected in accounting, read the article “Organization of cash desk operations in accounting (nuances)” .

Features for e-readers

Filling out the cash book manually is becoming less and less common, as many companies prefer to switch to electronic document management. Therefore, this document is filled out electronically. To complete this process correctly, the following rules are taken into account:

- as soon as the document is completely filled out, it must be printed;

- printed documentation is stapled and signed by the director of the company;

- if the responsible person in the company is responsible for maintaining the cash register in electronic form, then it is allowed to register the book quarterly;

- entries must be made daily by a designated person;

- The balance of money in the account must be indicated at the beginning of the day, and at the end of the day the total is summed up based on the transactions performed for one day of work;

- any transactions carried out during the day must be indicated in the book.

The advantages of using the electronic version include the fact that if the cashier makes any mistake for various reasons, it can be easily and quickly corrected.