Account 69 in accounting

Using account 69, information about the company’s employees is summarized by:

- Social insurance;

- Pension provision;

- Compulsory health insurance (CHI).

The accounts reflect the amounts to be transferred to the relevant funds on the credit side, and the transferred amounts on the debit side.

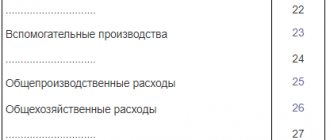

A separate sub-account is opened for each type of contribution in this account. The main subaccounts are presented in the figure:

An organization can open additional sub-accounts if there are payments for other types of social insurance and security.

Organization of accounting for account 69

An enterprise that makes payments to employees in accordance with concluded employment contracts is obliged to record the accrual of insurance premiums for their subsequent transfer to an extra-budgetary fund. The law provides for compulsory medical, social and pension insurance for employees. The employer must also ensure payment of insurance premiums in case of occupational diseases and accidents at work.

To reflect the amounts of accrued and paid contributions to extra-budgetary funds, account 69 is used. To analyze and control the amounts of contributions, the organization can open sub-accounts in accordance with the types of transfers made.

Regulatory documents provide that account 69 can be used to reflect the following transactions:

- calculation of the amount of contributions (including fines, penalties);

- payment of the amount of contributions (fines, penalties);

- reflection of expenses for contributions to extra-budgetary funds.

It should be noted that on account 69 not only the amounts of obligations to the funds are recorded, but also credits coming from the Social Insurance Fund are made.

Typical transactions for account 69

The main entries for account 69 “Calculations for social insurance and security” are discussed in the table:

| Account Dt | Kt account | Wiring Description | A document base |

| 69 | 51/52/55 | Transferring payments through a bank | Payment order |

| 69 | 70 | Calculation of benefits to an employee from extra-budgetary funds (illness/work injury/pregnancy and childbirth, etc.) | Help-calculation |

| 99 | 69 | Penalties for late payments | Help-calculation |

| 73.03 | 69 | Penalties for the payment of insurance premiums to extra-budgetary funds were withheld from the guilty employees of the enterprise | Act, certificate-calculation |

| 51/52 | 69 | Reflects the amount received if expenses exceed payments | Bank statement |

Typical transactions for account 69 in the table

The correspondence used with account 69 is fixed in the chart of accounts approved by the above-mentioned Order of the Ministry of Finance No. 94-n. Here are the most common wiring:

| Debit | Credit | Business transaction |

| On account credit 69 | ||

| 08 “Investments in non-current assets” | 69 | Insurance premiums are calculated from wages when creating an OS object on your own |

| 20 "Main production" 23 “Auxiliary production” 25 “General production expenses” 26 “General business expenses” 44 “Sales expenses” | 69 | Insurance premiums are calculated from:

|

| 28 "Defects in production" | 69 | Insurance premiums are charged from wages for repairing marriages |

| 51 “Current accounts” | 69 | Sick leave was reimbursed from the fund |

| 91 “Other income and expenses” | 69 | Insurance premiums are calculated from non-production premiums |

| 96 “Reserves for future expenses” | 69 | A reserve has been created for vacations in terms of accrued insurance premiums |

| 99 "Profits and losses" | 69 | Penalties and fines were accrued for late payment of insurance premiums |

| By debit of account 69 | ||

| 69 | 51 “Current accounts” | Insurance premiums transferred to the budget |

| 69 | 70 “Settlements with personnel for wages” | Amounts accrued to the employee on sick leave |

| 69 | 73 “Settlements with personnel for other operations” | Part of the cost of issued vouchers was written off from the Social Insurance Fund |

Account 69 “Calculations for social insurance and security”, as a rule, has a credit balance, showing the debt of the organization. If a debit balance arises, this means that the funds have a debt to the organization.

A debit balance on account 69 is more often inherent in social insurance calculations, when the amount of accrued contributions is less than the amounts paid to staff through social insurance payments (sick leave, maternity benefits, etc.)

Examples of operations on account 69 for dummies

Example 1. Calculation of insurance premiums

Renas LLC built the warehouse with its own resources. The total salary of workers involved in construction is 21,000 rubles. Insurance premiums of Renas LLC amount to 30%, including pension (22%), social (2.9%) and medical (5.1%).

Posting table – Reflection of insurance premiums from employees’ salaries (construction of fixed assets) in account 69:

| Account Dt | Kt account | Transaction amount, rub. | Wiring Description | A document base |

| 08.03 | 70 | 21 000 | Calculation of wages for construction workers. | Payroll |

| 08.03 | 69.01.01 | 609 | Calculation of contributions to the Social Insurance Fund | Payroll |

| 08.03 | 69.03 | 1 071 | Calculation of contributions for compulsory medical insurance | Payroll |

| 08.03 | 69.02 | 4 620 | Accrual for compulsory pension insurance | Payroll |

Accounting entries with account 69

There are not so many transactions in which the designated account can be used. The PBU presents the following operations:

| Debit correspondence | Loan correspondence | the name of the operation |

| 69 | 51/52/55 | The accrued amount of contributions is transferred from the current account to a specific department |

| 69 | 70 | The employee has received sickness benefits, maternity benefits, or other social benefits |

| 99 | 69 | Penalties are charged for late amounts transferred |

| 73.03 | 69 | Penalties were withheld for the payment of insurance premiums from company employees guilty of violation |

| 51/52 | 69 | The amount credited to the account as an excess of the company's expenses for social benefits to employees |

In the balance sheet, the balance of account 69 is reflected in the section of settlements with debtors and creditors. The account balance is included in the total cost.

Typical accounting entries for account 69

Debit entries:

D69 K50 – vouchers issued from the cash desk to employees paid by the Social Insurance Fund.

D69 K51 – the amounts of insurance contributions to funds from the current account are transferred.

D69 K70 – payments to employees are accrued from social insurance funds .

Loan transactions:

D20 K69 - contributions payable to the funds for employees of the main production for compulsory medical insurance, compulsory social insurance and compulsory health insurance are accrued.

D23 K69 – contributions were accrued to employees of auxiliary production .

D25 K69 – contributions payable to shop workers.

D26 K69 – contributions payable to management employees.

D44 K69 – contributions are accrued for payment for employees of trade organizations and those involved in the sale of products.

D99 K69 – amounts of penalties and fines were accrued to the Pension Fund, Social Insurance Fund and Compulsory Medical Insurance Fund.

D51 K69 – the funds returned the overpaid amounts of insurance payments.

D70 K69 – the amount of the voucher is withheld from the employee’s salary, received at the expense of the Social Insurance Fund.

| Working with account 69 involves paying contributions to the Pension Fund, Social Insurance Fund and Compulsory Medical Insurance Fund. Click and read: Payments of individual entrepreneurs to the Pension Fund and the Compulsory Medical Insurance Fund. Registration of individual entrepreneurs in the Social Insurance Fund and TFOMS. |

Account credit balance 69

Social insurance tax is calculated on the credit of the account, so the initial balance in the credit will indicate the presence of debt to the state under the Unified Social Tax. Each of the subaccounts has a separate balance, which makes it easy to see which payments were not made.

At the end of the reporting period, the credit balance indicates the total amount of debt for mandatory payments to the budget and the Pension Fund. After calculation, the data is transferred to the liability side of the balance sheet and reflected in the financial statements of the enterprise.

Typical wiring

Key transactions for the designated position are recorded using the following accounting entries:

1) Dt 69

Kt 51 – transfer of insurance contributions to an extra-budgetary fund;

2) Dt 20

Kt 69 – insurance premiums for employees of primary production;

3) Dt 44

Kt 69 – calculation of insurance premiums for employees responsible for ensuring the process of product sales;

4) Dt 51

Kt 69 – return by extra-budgetary funds of overpaid funds, etc.

Table of typical transactions for account 69

The basis for calculating the amount of insurance premiums is the amount of remuneration that is paid to the employee according to the employment contract. The amount of accrual of contributions is carried out according to Kt 69, transfers to extra-budgetary funds are reflected in Dt 69. Also, according to Kt 69 the amount of receipts of contributions credited from extra-budgetary funds in favor of the organization can be carried out.

Basic transactions on account 69 are reflected in accounting with the following entries:

| Dt | CT | Description | Document |

| 69 | Insurance premiums are transferred to an extra-budgetary fund | Payment order | |

| 20 | 69 | Insurance premiums accrued to an employee of the main production | Payroll |

| 44 | 69 | Insurance premiums have been accrued to the employee who ensures the process of selling goods | Payroll |

| 99 | 69 | Accrual of fines and penalties for insurance premium payments | Accounting certificate-calculation |

| 69 | Refund of funds overpaid to extra-budgetary funds | Bank statement |

In what cases is count 69 applied?

Posting Dt 69 Kt 69 “Calculations for social insurance and security” is used to reflect debt and its repayment to extra-budgetary funds.

In accordance with the instructions approved by the order of the Ministry of Finance of the Russian Federation “On approval of the Chart of Accounts for accounting financial and economic activities” dated October 31, 2000 No. 94n (hereinafter referred to as the Instructions), the following sub-accounts can be opened for account 69:

- 69.01 - for accumulating payments to the Social Insurance Fund,

- 69.02 - shows the amounts accrued and paid to the Pension Fund of Russia,

- 69.03 - reflects the debt to the Federal Compulsory Medical Insurance Fund.

It should be noted that the payer of contributions can provide his own analytics of account 69 taking into account the chart of accounts used in the organization.

About state social funds

It is worth noting that as such the concept of UST (unified social tax) no longer exists today. Accountants use the abbreviation out of habit. The tax itself was abolished on January 1, 2010. Instead, mandatory social insurance payments were introduced into the relevant funds. The general principles of accrual and payment remain unchanged.

Let's consider the main state social insurance funds and their purpose:

- PF - pension fund - off-budget state, intended for payment of funds after the end of employment upon reaching retirement age, for length of service or upon the loss of a breadwinner.

- FSS - the social insurance fund - guarantees payments in case of accidents, payment of sick leave and maternity benefits. In addition, it finances certain types of health resort trips.

- FFOMS - the federal compulsory health insurance fund - allows you to use guaranteed medical care services.

The company transfers funds to each fund separately, for which it opens account 69 and the corresponding sub-account transactions.

What is account 69 used for in accounting?

The law obliges every employer to pay contributions to social funds on almost all remunerations (salaries) of its employees. Let's look at what it is.

Contributions to the funds are mandatory payments that guarantee each employee medical care, pensions, and insurance compensation in case of disability.

There are currently four types of such contributions:

- To the Pension Fund;

- To the social insurance fund - divided into two, payment of disability and compensation for injuries;

- To the health insurance fund.

Attention!

Since 2020, the Federal Tax Service has been managing these contributions (except for injuries). They are transferred by the 15th of each month in separate payment orders. To carry out accounting of accrued and paid amounts for each type of contribution in the chart of accounts, account 69 “Calculations for social insurance and security” is used. Since this information is widely used to fill out various reports, it is necessary to organize accounting in the context of each fund, as well as the type of transfer to it (contribution, fine, penalty, etc.).

Postings to account “69.03.1”

By debit

| Debit | Credit | Content | Document |

| 69.03.1 | 51 | Transfer of funds from the organization's current account to pay off debts to the budget for insurance premiums in the part transferred to the federal compulsory medical insurance fund | Debiting from current account |

By loan

| Debit | Credit | Content | Document |

| 000 | 69.03.1 | Entering initial balances: insurance premiums in the part transferred to the federal compulsory medical insurance fund | Entering balances |

| 20.01 | 69.03.1 | Inclusion in the costs of the main production of the amount of insurance premiums in the part transferred to the federal compulsory medical insurance fund | Payroll |

| 23 | 69.03.1 | Inclusion in the costs of auxiliary production of the amount of insurance premiums in the part transferred to the federal compulsory medical insurance fund | Payroll |

| 25 | 69.03.1 | Write-off of the amount of insurance premiums to general production expenses in the part transferred to the federal compulsory medical insurance fund | Payroll |

| 26 | 69.03.1 | Write-off for general business expenses the amount of insurance premiums in the part transferred to the federal compulsory medical insurance fund | Payroll |

| 29 | 69.03.1 | Write-off for expenses of service industries and farms the amount of insurance premiums in the part transferred to the federal compulsory medical insurance fund | Payroll |

| 44.01 | 69.03.1 | Inclusion in distribution costs of the amount of insurance premiums in the part transferred to the federal compulsory medical insurance fund in organizations engaged in trading activities | Payroll |

| 44.02 | 69.03.1 | Inclusion in business expenses of the amount of insurance premiums in the part transferred to the federal compulsory medical insurance fund in organizations engaged in industrial and other production activities | Payroll |

| 91.02 | 69.03.1 | Inclusion in other expenses not related to the main activities of the amount of insurance premiums in the part transferred to the federal compulsory medical insurance fund | Payroll |

| 96.01.2 | 69.03.1 | Write-off of the estimated liability (use of the reserve) for the cost of contributions in the part transferred to the Compulsory Medical Insurance Fund | Payroll |

| 96.01.2 | 69.03.1 | Write-off of the estimated liability (use of the reserve) for the cost of contributions in the part transferred to the Compulsory Medical Insurance Fund (accounting for wages in an external program) | Reflection of salaries in accounting |

Why do you need SALT according to account 69?

The law does not allow accounting outside of accounting registers (clause 3 of Article 10 of Law No. 402-FZ of December 6, 2011 “On Accounting”). One of the accounting registers is the balance sheet for account 69 “Calculations for social insurance and security”. It accumulates information on settlements with extra-budgetary funds (FSS, Pension Fund, Compulsory Medical Insurance Fund) during the reporting period.

Without using this statement, it is impossible to generate data for the reporting period on accrued and paid insurance premiums, that is, to adequately judge the state of mutual settlements with these funds.

Without SALT according to the account. 69 it will not be possible to draw up a balance sheet that reliably reflects the company’s receivables and payables in terms of payments for social insurance and security.

Inspectors almost always request SALT during inspections and have the right to fine company officials under Art. 15.11 Code of Administrative Offenses of the Russian Federation in the absence of accounting registers.

The law qualifies the absence of accounting registers as a gross violation of one of the requirements for accounting, the fine for which can range from 5,000 to 10,000 rubles, and in case of repeated violation - up to 20,000 rubles.